IR Playbook

Maximizing your return on time

In this report, IR Impact looks inside time management, with real-world examples of how leading IR professionals manage their workloads

IR has been subject to ‘job creep’ in recent years, with the average IRO increasingly taking on ‘non-core’ activities

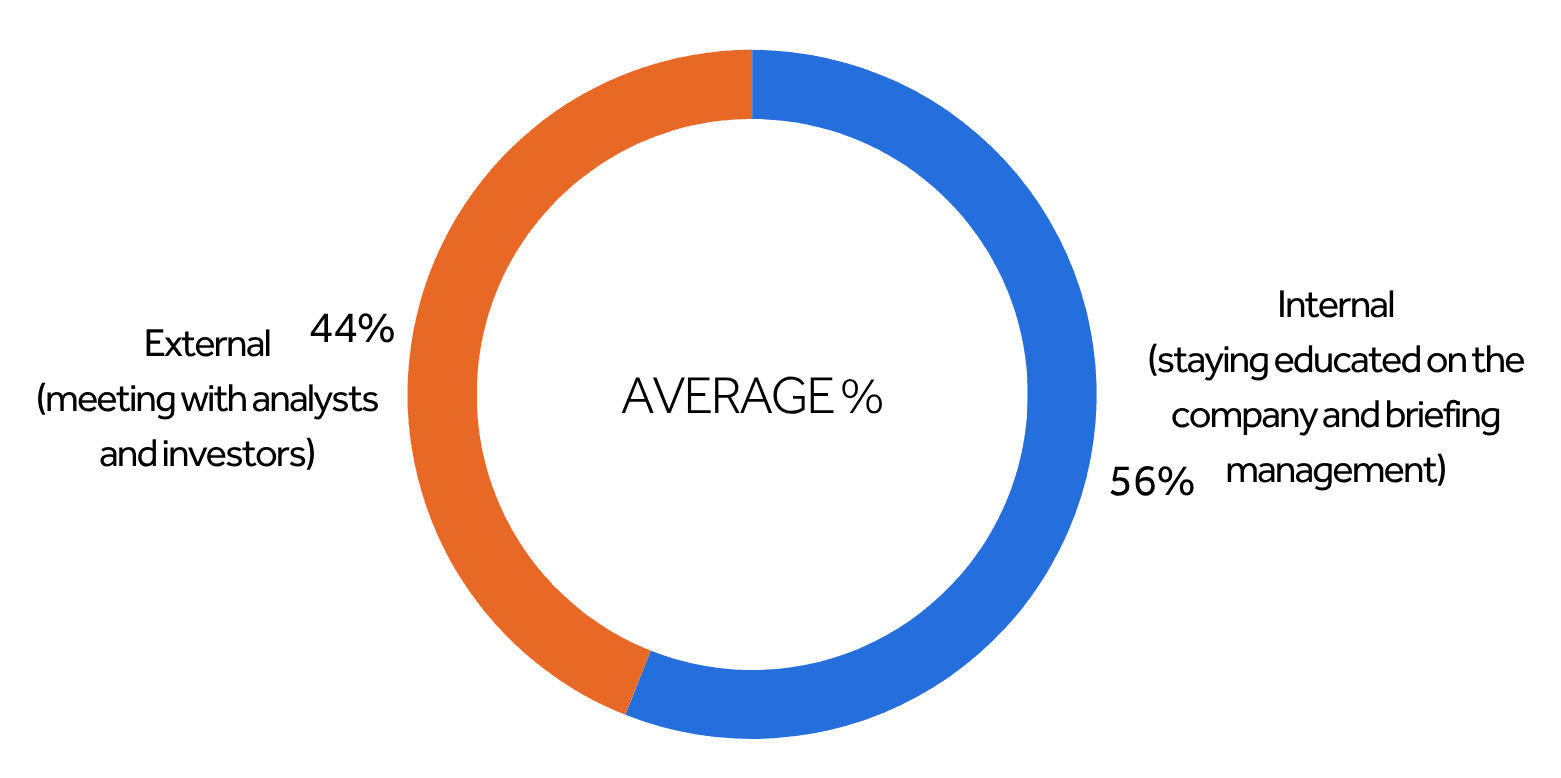

While it is often seen as an outward facing function, more than half of an IRO’s time is spent on internal work, with earnings preparation deemed most important as well as being the task that takes up the most amount of IR time

After that, it is activities around the board and management – going on the road, internal briefings – that are considered most important and that take up more time

ESG is something of a conundrum. An area that has increasingly fallen under the remit of IR in recent years, it is largely considered the least important IR task, despite the many column inches dedicated to it, the mammoth regulations and the many hours spent on ESG

Some tasks lend themselves to efficiencies more so than others. The earnings process is a clear place to start, with a slew of tools and solutions that can speed up the quarterly merry-go-round as well as improving understanding and output. By streamlining something that is a non-negotiable essential, IR leaders give themselves back more time for building and nurturing relationships – be those with management, the board or the Street.

If the last 30 years saw the IR function evolve from a financial reporting or communications role to a highly strategic function that can deliver game-changing relationships with the Street, what do future decades hold?

That is a hard question to answer given the vast potential offered by AI – something investor relations professionals are only really beginning to explore. What is already clear however, is that the first port of call for AI in IR is to carry some of the load and streamline time-heavy tasks, freeing up precious resources for the jobs that deliver the biggest return on investment.

And the AI revolution couldn’t come at a better time: research by IR Impact shows that IROs are increasingly taking on tasks outside of the traditional investor relations role, from corporate access (53 percent) to ESG and sustainability (49 percent), corporate communications (40 percent) to corporate strategy (28 percent) and more.

These non-core deliverables are typically time heavy – think about the growth and scope of ESG alone – leaving IR doing more even as resources fail to match pace. However, these are also some of the areas where the right tips and tricks – and a sprinkling of tech – can deliver real time saves.

In this playbook, written in association with Notified, we look at how IROs divide their time and what tasks they consider most valuable.

We explore the work that demands the greatest resources – and look at how that compares to the tasks IR professionals say deliver the greatest value to their company. Through an exclusive survey we weigh up spending time internally versus externally, look at the importance that IROs place on different deliverables and consider how their priorities have changed over recent years.

Diving even deeper behind the numbers, we speak to award-winning, senior IROs about the tools they put to work to ease that ever-increasing workload and free up as much time as possible for the relationship building that is the cornerstone of investor relations.

Blake Fernandez, vice president of IR at Plains All American

Peter McGough, senior vice president of IR and capital markets at Gambling.com

Claire Mogford, head of IRat SEGRO

Romas Viesulas, head of IRat Vista Alegre.

IR is all about relationships – both internal and external. It’s easy to think of the investor relations role as being all about those crucial buy-side and sell-side engagements, but IR Impact research shows that it is actually the internal part of the role that people dedicate the most to, with respondents saying they typically spend 56 percent of their time to educating themselves internally and updating management and the board. That leaves slightly less than half of an IRO’s time left for those external engagements that are the bread and butter of IR.

This time spent on the internal side of investor relations can come as a bit of a surprise to some entering the profession too: when IR Impact spoke to former sell siders about their move into the corporate world, this was the area that they said required the most adjustment. It is also something highly company-specific, with much depending on where the firm is in its lifecycle or its earnings cycle, as well as how management approaches investor relations.

The external piece – talking to investors and all the blocking and tackling – is what [us former] sell-side analysts are used to. What’s unique to each company is the nuance of working with that management team and the internal aspects of navigating through the organization. At Plains, my time is probably split 60 percent internal, 40 percent external and that essentially evolves around earnings. In that quiet period and during that prep, you’re completely focused on internal work: getting the numbers together, preparing press releases, PowerPoint presentations and meetings with senior management. After that, it shifts to being out on the road, telling the story.

My time is increasingly moving internal versus external, because I’m not just IR – I help out with the capital structure of the of the firm too. Then there’s the fact that when I joined, there were about 300 employees. There’s now 600. So there’s more to do in terms of corporate comms, in terms of preparing the messaging for not just earnings, but other kinds of relevant news events, like acquisitions and the impact on the model.

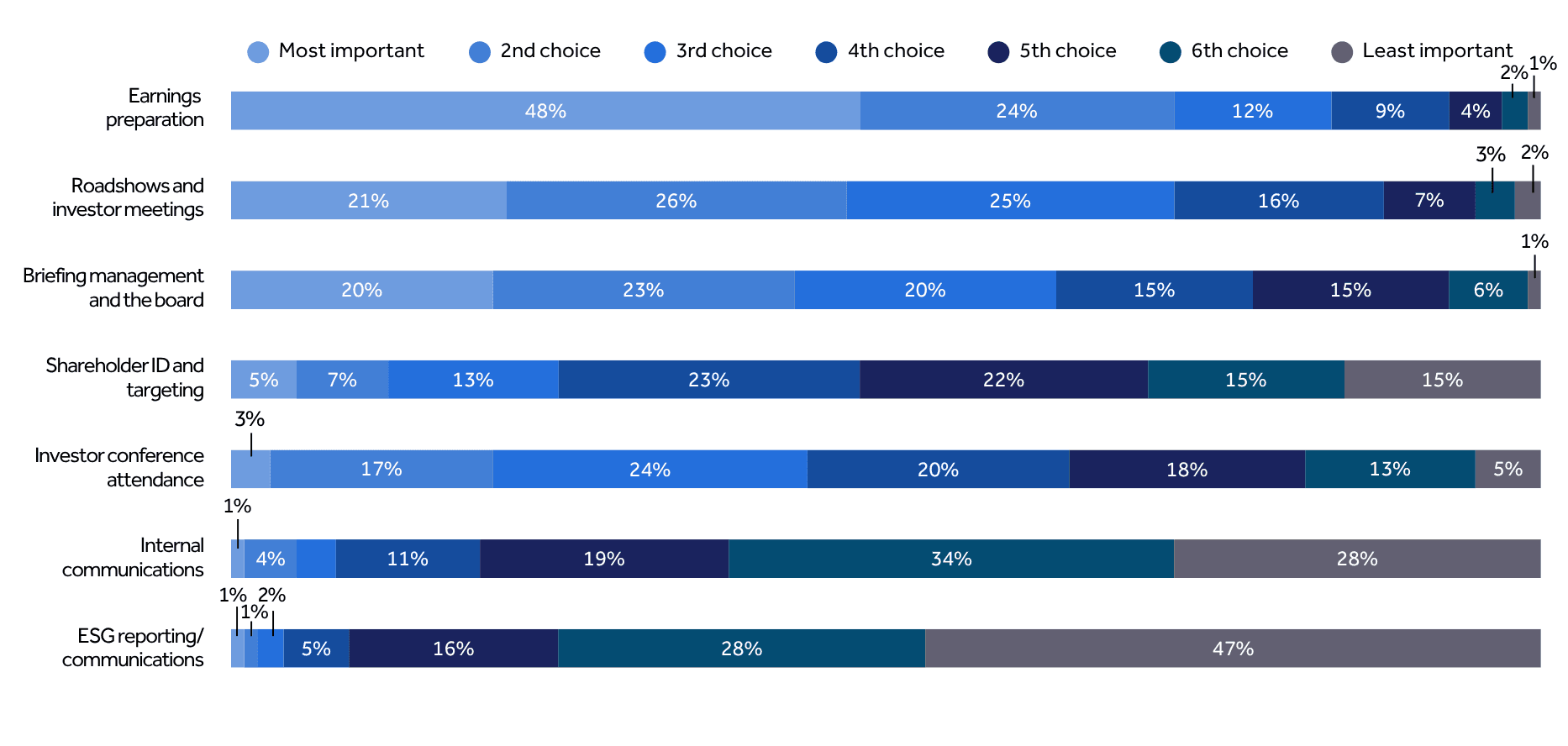

Our survey of the IR community shows that IROs not only spend more time internally but typically rank these internal activities as among the most important work they do. When asked to rank a group of activities by importance, almost half (48 percent) of respondents put earnings preparation in the top spot. This is of course an endeavor that will ultimately become outward facing as companies report to the market, field calls with analysts and investors and go on the road. The preparation side is not only internal but a task that requires a concerted effort and much cross-department collaboration. It is also an area where tech is really driving efficiency.

I use AI for notetaking and some transcription and, as far as keeping the CRM updated, that has been a significant time saver. I’ve also experimented with AI to clean up quotes or help with word choice or tone for press releases. This was the first quarter where there was an incremental speed up in my process. Of course, the process around earnings preparation or press releases has to happen. You have to do it. But we’re still a $500 mn market cap company – one that is extremely profitable – and we have a lot of education to do. The most valuable thing I can do is speak to a new constituency, investor, analyst or banker to get that message out there.

The results process and the reporting process is hugely time consuming. It’s literally four weeks full-on, head down. There’s a lot of number crunching to get to the data that you need and a lot of time spent finessing the messaging. It’s important because it’s got a regulatory element to it, but it is an area where we are looking at how we can put in a lot more in the way of efficiency and streamlining that process – particularly on the verification side.

We use different software applications for targeting as well as tracking shareholder changes. When we go on the road and meet with investors, that all goes into the application, so we have easy access to go back and see: when was the last time we met with these folks? How many shares have they bought or sold over that timeframe? We’ll also run our earnings script through AI to see what the output looks like and to make sure there’s no real negative screening.

Help with logistics: planning, itineraries and schedules would be great, If there’s an AI logistics bot coming down the road, that would be very helpful for me.

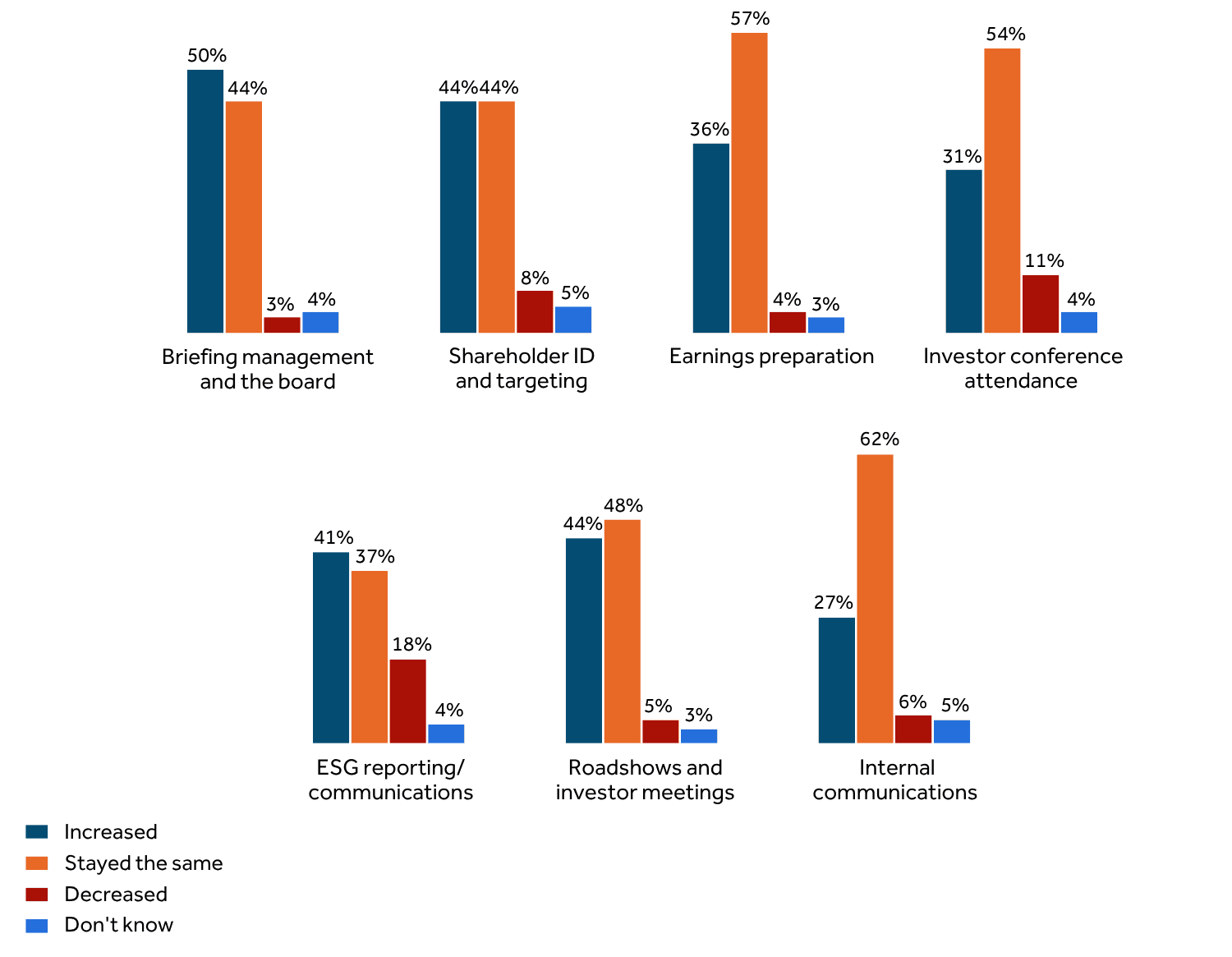

Roadshows and investor meetings are considered the second most important activity (21 percent), but these are closely followed by another internal-facing essential: briefing management and the board. None of the remaining tasks got a notable vote as the most important IR activity, though things shift a bit when we move further into the top three, with investor conference attendance and shareholder ID also getting a look in as we move to the second and third most important IR activities.

I spend a lot of time on calls with analysts but I wouldn’t ever say that’s a waste of time, because it’s very important to make sure they’re helping tell the story. I also spend a lot of time on calls with potential shareholders – some of them quite small. Is there a way of making that more efficient? Maybe. But the reality is you never really know which one’s going to end up being a big shareholder and which isn’t. I see my job as a kind of filter for management: I do all those initial calls, and then I’ll arrange follow ups with the CFO for the best leads.

In our research, we also asked IR professionals to rank those tasks that they consider least important. While not the area they spend the most time on, ESG can be a huge ask – from questionnaires, an IR burden for more than a decade already, to the proliferation of frameworks and regulation such as CSRD. And it is by far the area that IROs see as having less importance (47 percent).

I’d say that the most time-consuming task is ESG reporting related. Often, it’s fairly generic – the sort of data points you might expect – but it feels like a lot of requests are just ever so slightly different or the data I receive isn’t in quite the right format, so it requires attentive review and that can take up a lot of time. ESG has also become a much more insistent question from analysts: at least as important as the quarterly earnings cycle and, as we don’t yet have a dedicated sustainability officer, a lot of that falls to me.

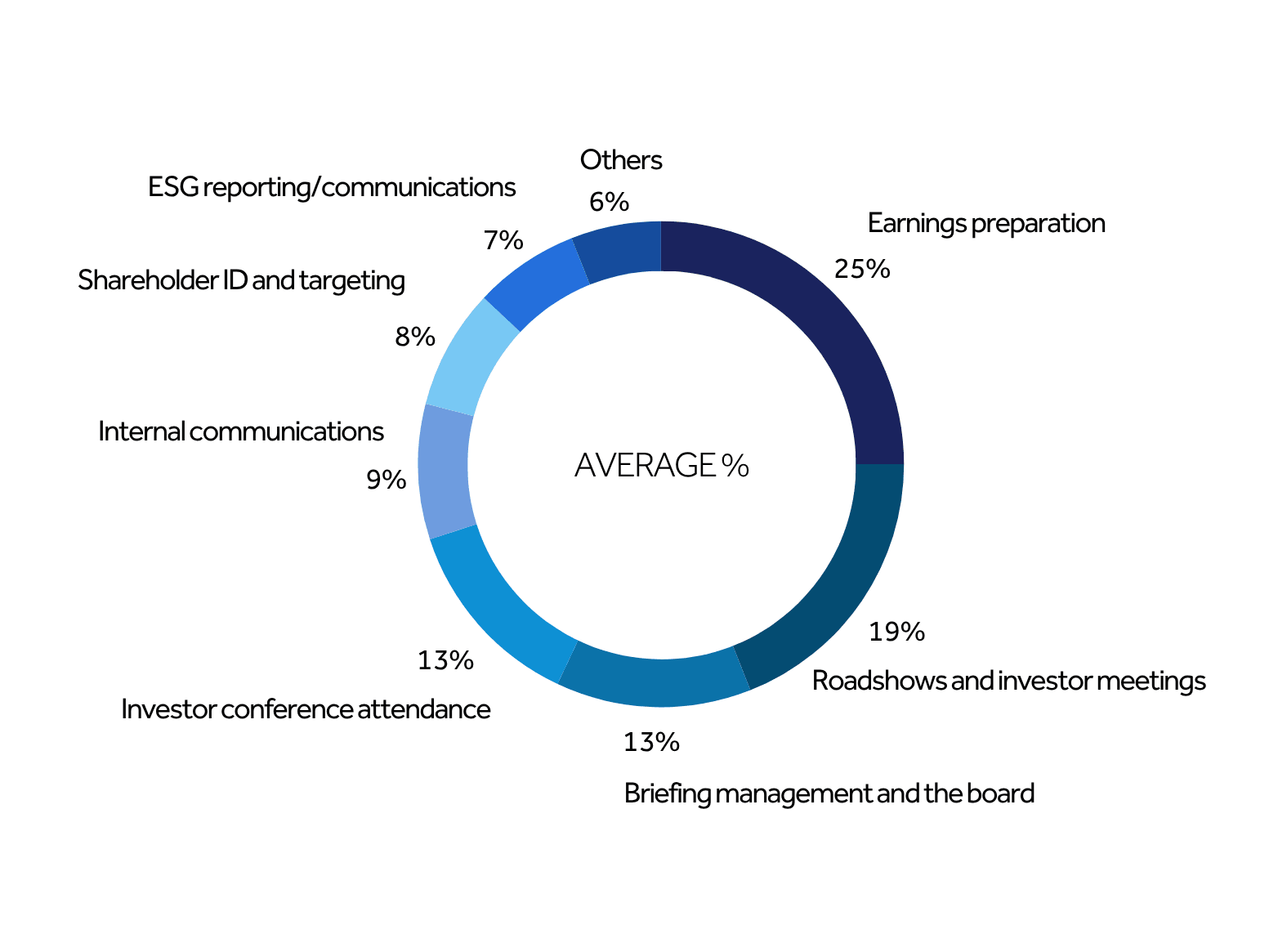

Looking at how much time IROs spend on different tasks, we see – unsurprisingly – that the most hours are dedicated to those areas deemed most important. Earnings prep takes up around a quarter of the average IRO’s time – even outside of the US where companies aren’t always tied to a quarterly earnings cycle. Although roadshows and investor meetings rank almost equal to management and board briefing when it comes to importance, these activities rightly take up more of an IRO’s time given what’s involved. IR professionals say they spend almost a fifth of their time on this type of corporate access, versus 13 percent on board and management briefings.

Coming in as a non-real estate expert, I quickly realized that our investment case was quite complicated – and very focused on the specialists. If we’re trying to get a generalist fund manager’s attention, we need a very simple story that picks on some key themes that they’re going to be able to understand quickly and then dig into further. We did a lot of work in my first 18 months around developing a separate presentation that we use for generalists, taking out a lot of that jargon and making the story very understandable.

Over on the ESG bandwagon again, respondents in our research say they spend 7 percent of their time reporting and communicating around this task – a disproportionate amount of time for a task just 4 percent ranked among the entire top three of the most important IR duties.

We’re never going to score highly because we’re in the gambling ecosystem. I don’t think it is a good use of time to spend 40 or 50 hours – between our general counsel team and myself – to go from a C minus to a C in a report that bases its ratings on scraping our website. I came from the sell side where primary research is important. The ESG ratings process is horribly incomplete.

As the IR role evolves and as companies increasingly look to their IR heads for insights on everything from shifting regulations to today’s highly unpredictable world of geopolitics and trade tensions, some tasks are gaining importance, while others are dropping down the list of priorities.

So what’s changed? We asked IR professionals how the importance of different activities had shifted over the last three years – and what really stands out is that briefing management and the board is of paramount importance.

Already a vital part of the IR function, half (50 percent) of all those polled say briefing management and the board is an area that has increased in importance – rather unsurprising given global events over recent years – and just 3 percent say it has decreased. Some segments stand out here: 60 percent of mid-cap companies say the IR interaction between the board and the C-suite had increased in importance, while high numbers of those in consumer staples (60 percent), consumer discretionary (63 percent) and communications (67 percent) agree.

Our year is very cyclical so some periods are very internally focused, but I probably spend 10-15 percent of my time internally. I do a weekly share-price email that goes to our board but also to our employees, who are all shareholders. They can see what’s going on after every set of results, through a market-response wrap-up, which will have key notes from analysts and takeaways related to the share price. Then, twice a year, I present to the board with a summary of what we’ve been doing, what key themes have come up and how we’ve addressed those as well as what we in IR think the board should focus on for the next six months. There’s quite a structure to it.

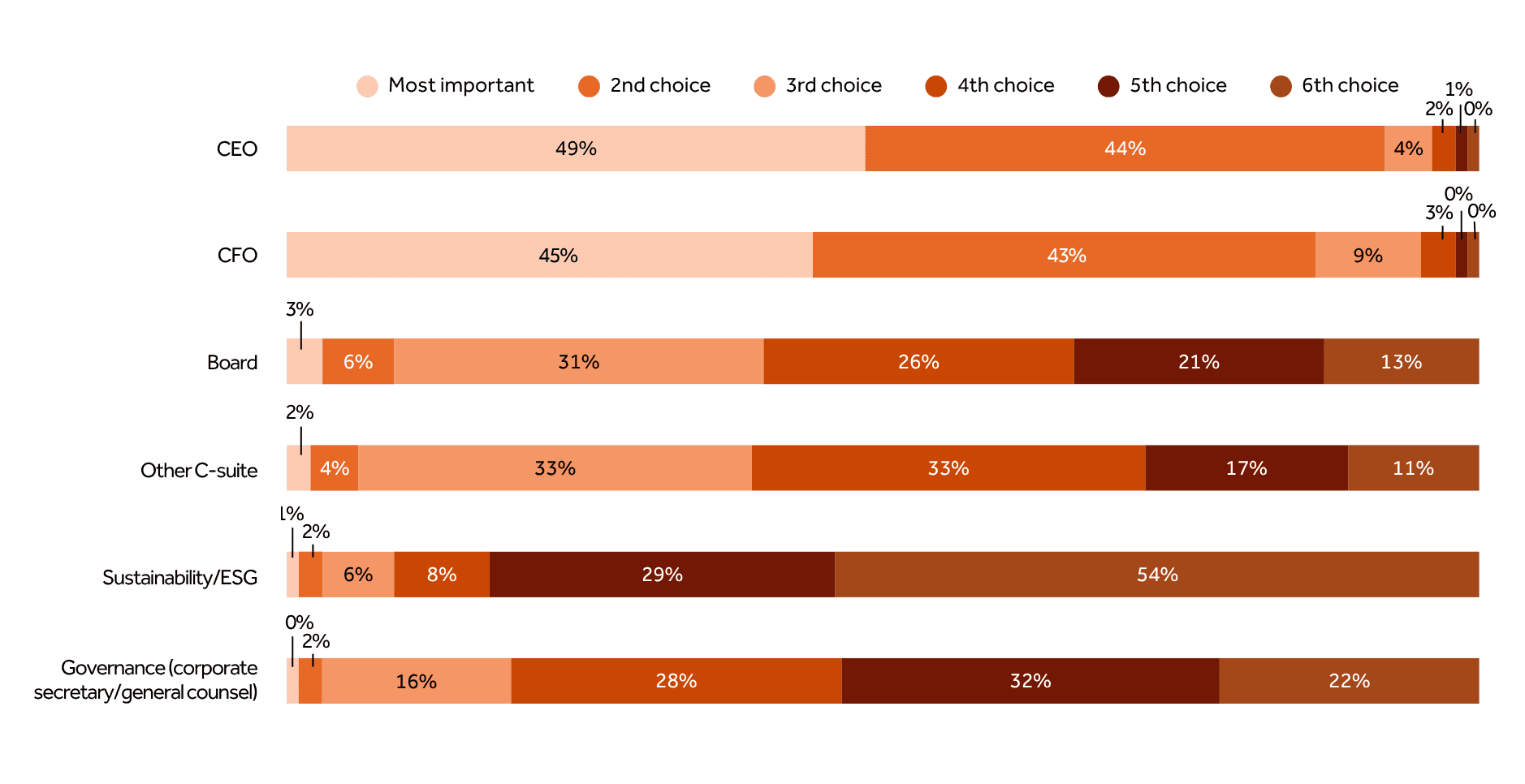

Given how important that IR-C-suite-board relationship is, we wanted to explore the different internal relationships that IR professionals rely on to deliver the information they need to the Street – and to communicate back to the company what the external perception is and where and when investor education is needed.

The data shows that relationships with the CEO and CFO are deemed most important. These are the executives that IROs report to, the management they travel with, the people they work through crisis and celebration with. And despite 75 percent of IROs reporting to the CFO last year – a figure that had jumped 9 percentage points in a single year – IR professionals consider their relationship with the CEO (49 percent giving their CEO relationship a number-one ranking) as being slightly more important than with the CFO (45 percent).

Interestingly, just 3 percent give their relationship with the board top ranking, climbing to 6 percent for second-place importance. It isn’t until we hit third place that there are any meaningful numbers here (31 percent). This suggests that in the responses covered previously – where IROs rated their briefings to management and the board as being of high importance – it is likely that it is the IR-to-C-suite relationship nudging that answer up the chart.

We don’t have a huge hierarchical structure – everyone here hotdesks for example – so I get to spend a lot of time one-on-one with both the CEO and the CFO, which means that a lot of our communication happens as part of that process.

My time is probably split 50/50 across proactively reaching out to investors or fielding their incoming calls and spending the other half of my time doing the reverse: keeping management informed of what the analysts are saying and the inbound we’re getting from investors.

What’s most important, frankly, is getting out and marketing. It is time consuming – especially for the senior management team because you’re basically taking the CEO or the CFO out of the office and on the road for multiple days. But it’s an investment. It’s about that bang for the buck and it is the way you get investors to trust you: by sitting across the table from the management team, looking into their eyes and getting to know the strategy.

An essential for any modern IR professional – and something that is a clear takeaway from IR Impact’s research – is the ability to identify those tasks where you can save time without compromising on the value they deliver to you, your IR program and your company.

Traditionally relative latecomers to the tech party – in part because of the highly regulated and sensitive nature of much that IROs deal with – investor relations leaders are increasingly picking up the bat for their companies around tech and AI, allowing them to become thought leaders and board educators as well as saving time and maximizing value across the IR program.

In fact, much of this is about doing things smarter as well as faster. IR heads across different cap sizes and sectors, those with lean or full coffers know that their peers are quickly catching on to the benefits of a new generation of IR solutions.

This is not just a keeping-up-with-the-Joneses situation: those making investment decisions have long been leaning on tech and the earnings process – hugely important but also representing a significant chunk of time – is a great example of where IR is catching up. Today’s generative AI tools can help you craft your message not just faster or in the tone your management wants to hit but also assess the output to gauge sentiment as well.

Efficiencies can also be found around those crucial internal relationships and interactions with the board and management – in the ad hoc way many briefings take place or around more formal external travel IROs undertake with the CEO and CFO. These trends – tech, AI, generative AI – are key themes and disruptors externally. IR must experiment, employ and understand these tools in order to best advise management and the board. From having data to hand, to sentiment analysis or tracking interactions and feedback with investors and analysts, seemingly simple time savers can make a huge difference to the kinds of feedback IR can provide and the ultimate value placed on the function.