Discover how IR teams across the globe are conducting roadshows

Laurie Havelock

Ash Govender

Tobi Ogunjemilua

Welcome to the 2025 edition of the IR Global Roadshow Report, proudly researched and compiled by IR Impact.

Investor roadshows play a crucial role in the financial ecosystem, acting as a bridge between companies and potential investors. These events – many of which are huge organizational undertakings – are designed to provide attendees a complete view of the investment opportunity ahead of them. Increasingly, roadshows are taking in interactive and other emerging digital formats, lasting for several days or taking in several countries en route.

This marks our 15th annual deep dive into corporate roadshow activity around the globe, as reported by IROs who responded to our surveys. After the last edition of the report presented an impression of how companies were conducting roadshows in a completely post-pandemic landscape, this year’s research shows several of those mid-term trends stabilizing and giving us a glimpse of what life on the road may be like into 2025 and beyond.

The past four editions of this report have examined both in-person and virtual roadshows, and this year’s is no different – both means of reaching investors have remained integral to most IR teams’ efforts. As a result, this report has an equal focus on virtual and in-person roadshow activity, covering frequency and duration, brokers used and cities visited. In some instances, comparisons between current and pre-pandemic activity have been provided. The report further covers the relative satisfaction IROs have with in-person and virtual roadshows.

As you will see, the exact trends here have shifted somewhat year-on-year. For example, the proportion of companies who undertook a roadshow in 2024 has grown since the year before, while the proportion of respondents who relied solely on a virtual event format has fallen. New cities are emerging among the most-visited destinations in the world, as have names among the most-used brokers for both physical and virtual events.

I’m not going to ruin any of those surprises, however: read on for the rest of the report to get a full picture of how IR teams are conducting their roadshows, split by market cap and region where possible.

You can also examine the findings of this report – and our entire back catalogue of research stretching back over decades – using IR Impact’s new digital benchmarking tool, which you can use to compare the findings of our survey against your peer group. I’d recommend having a play with it as soon as you can.

And – in the meantime – if you’ve undertaken a unique or particularly interesting roadshow, why not let us know? You can always email the IR Impact editorial team at editor@ir-impact.com.

Until next year!Laurie Havelock, Editor

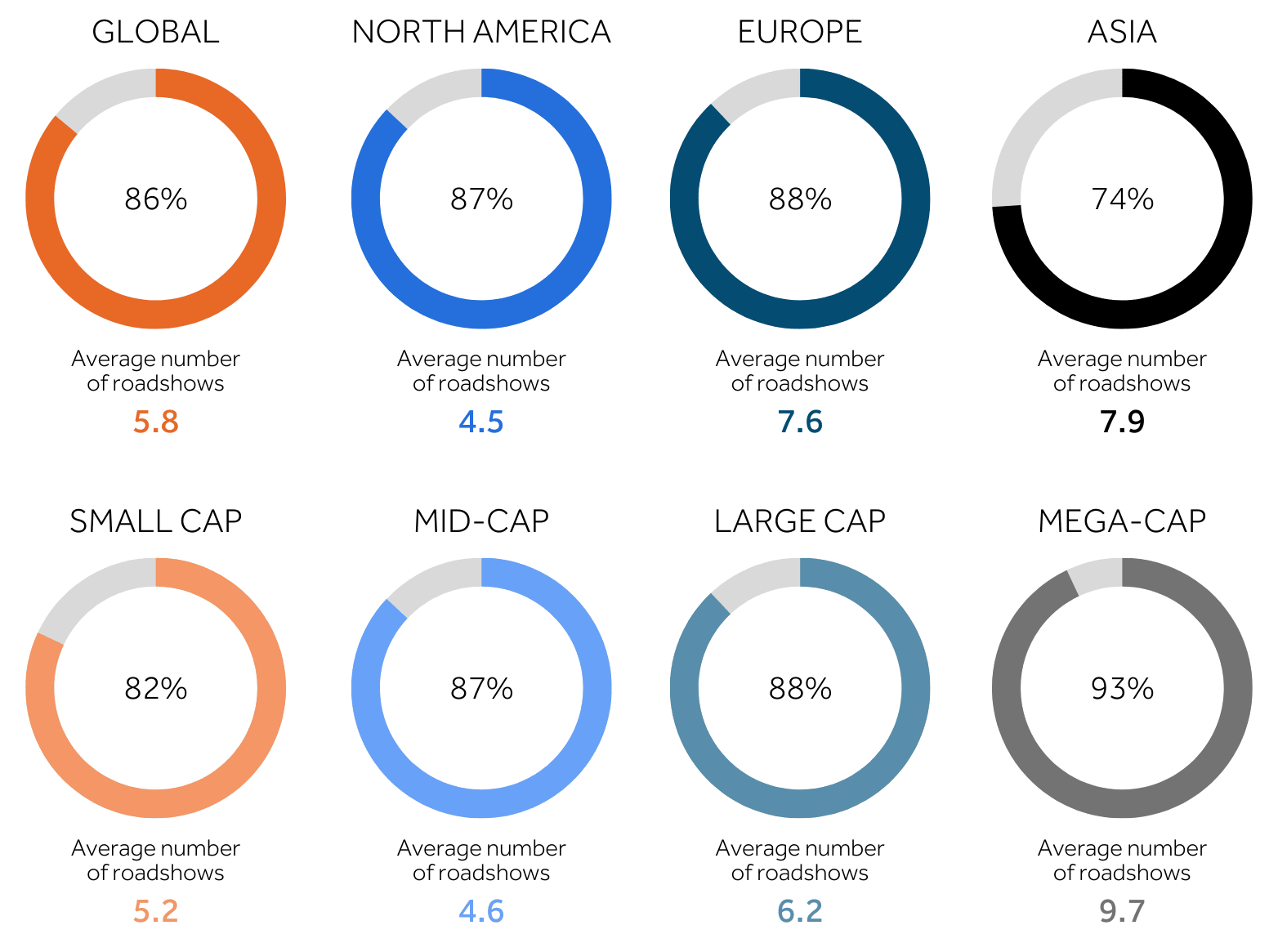

Eighty-six percent of companies across the globe embarked on an investor roadshow in 2024, compared to 84 percent recorded in the previous year’s report

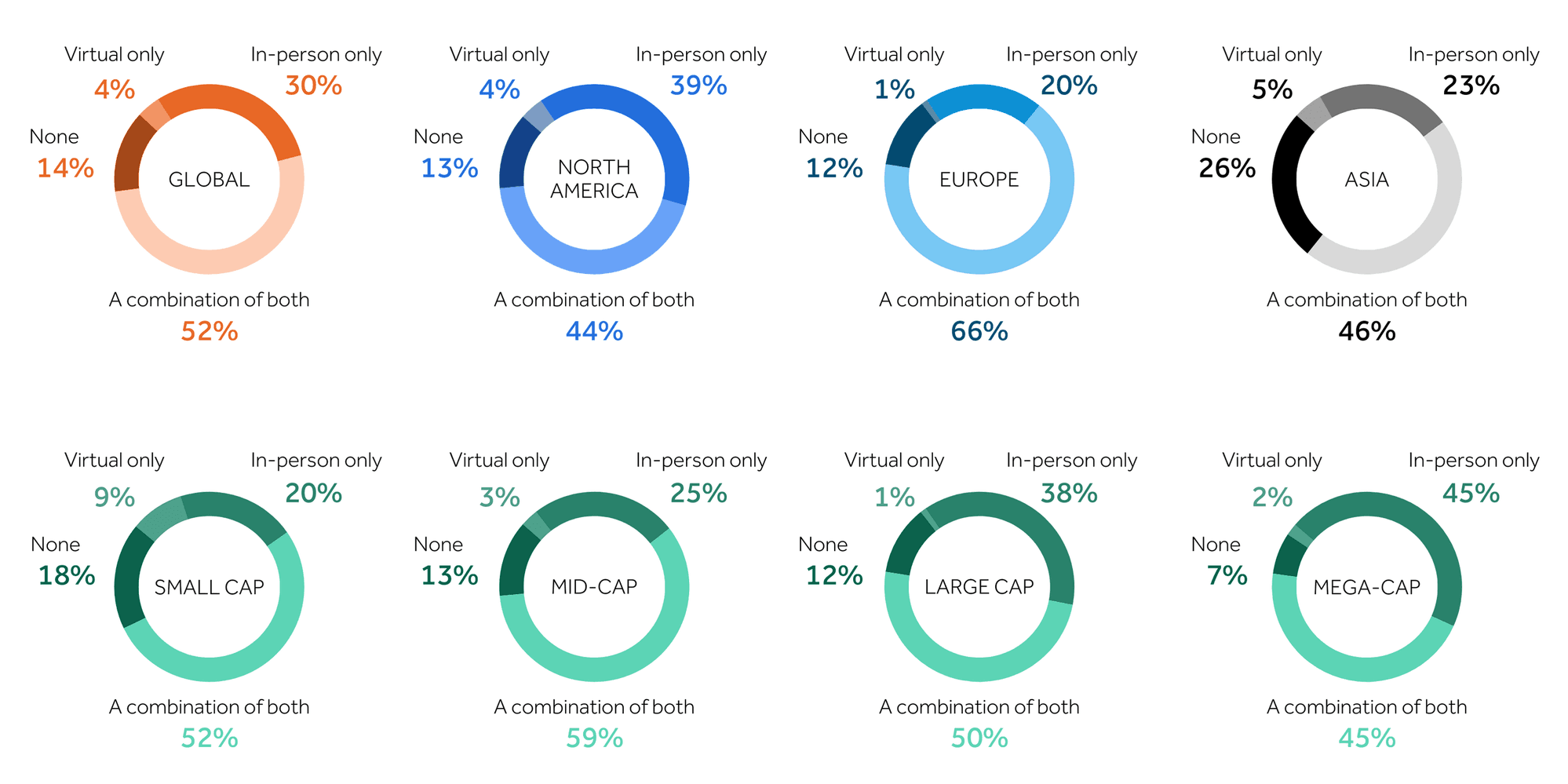

Overall, IROs are embracing in-person roadshows as their preferred method of meeting new investors, with the proportion of respondents saying they only rely on virtual events falling to just 4 percent in 2024

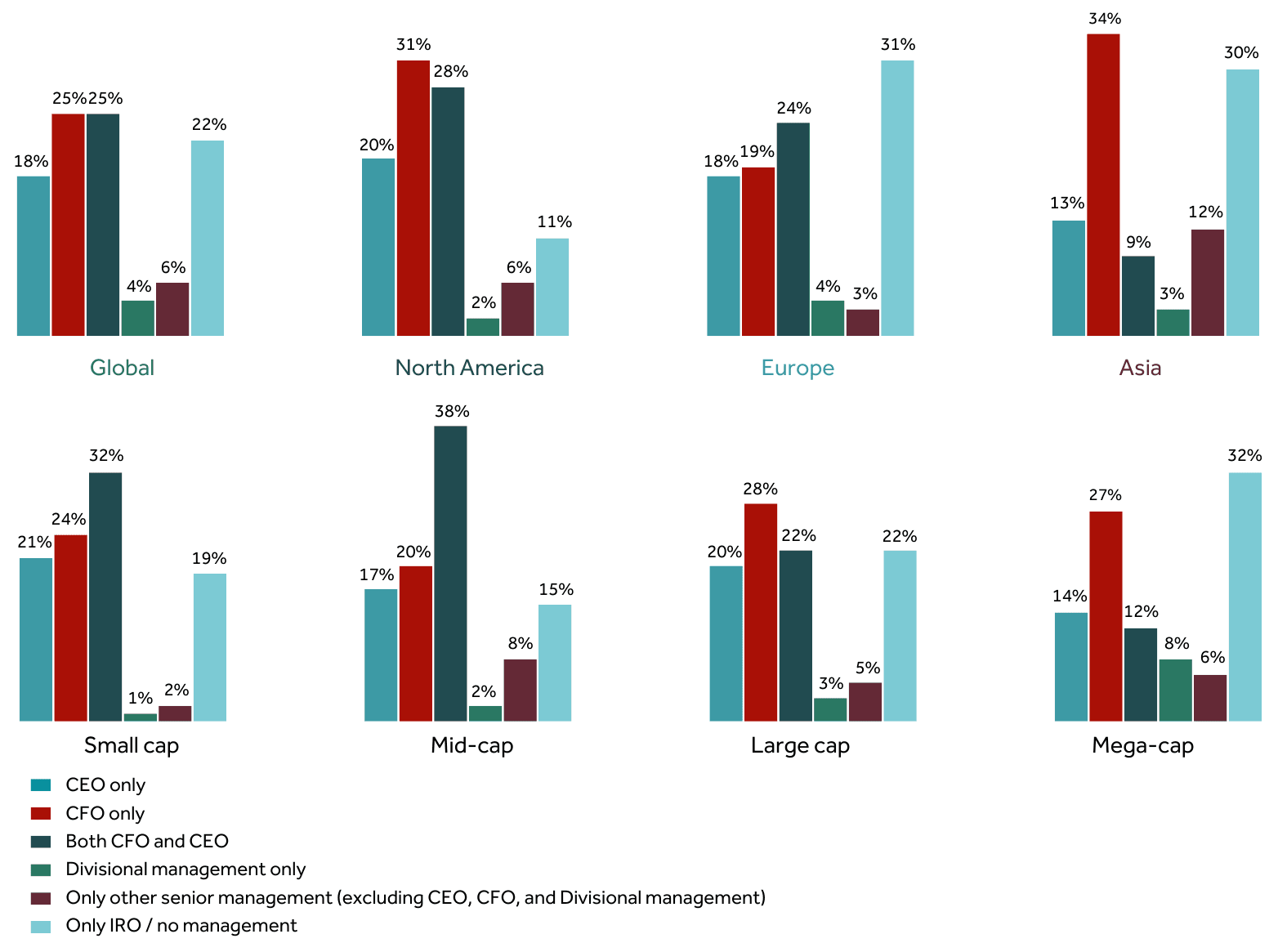

IR-only is on the up. The total proportion of in-person roadshows that had no management attending grew slightly (up to 22 percent). The total proportion of such events that had a CEO, CFO or both management figures attend fell to 68 percent)

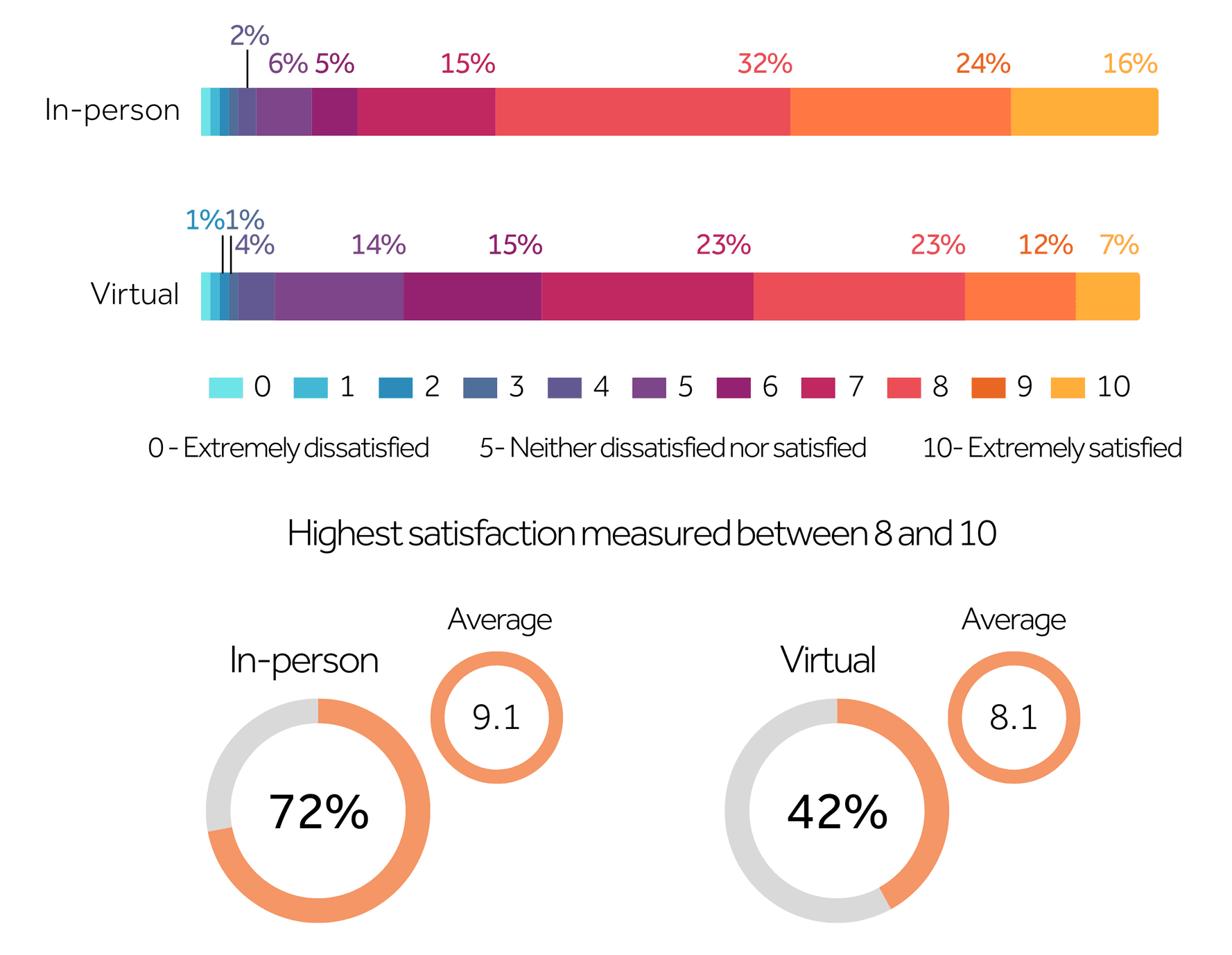

Almost three quarters of all those polled rated their satisfaction with in-person roadshows at between eight to 10 out of 10 – a matching the findings from 2023’s report

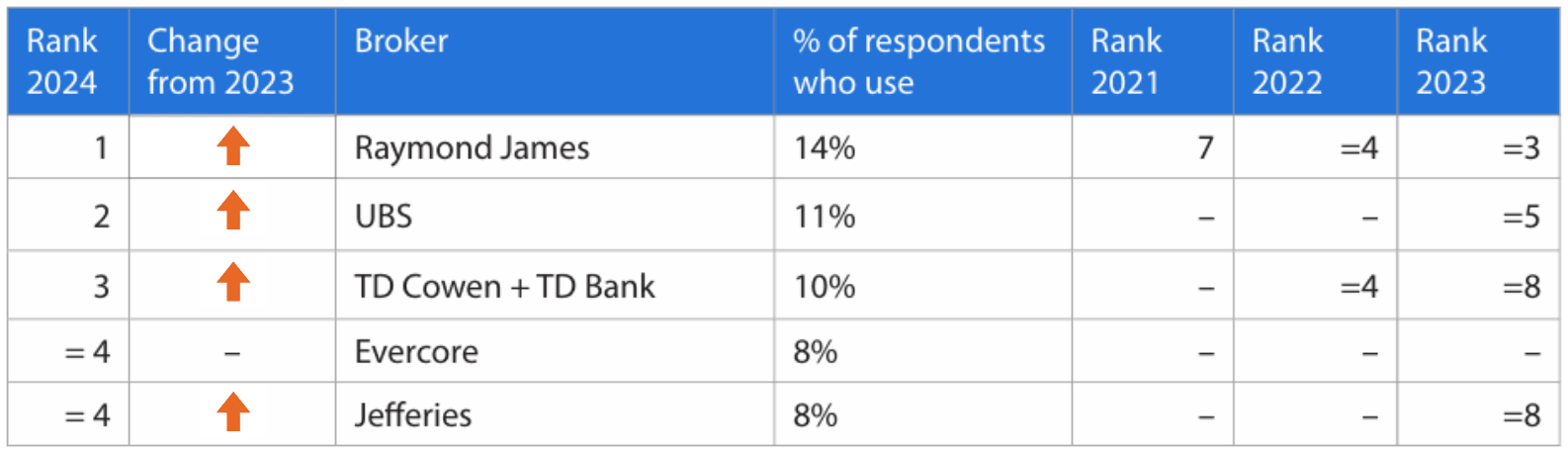

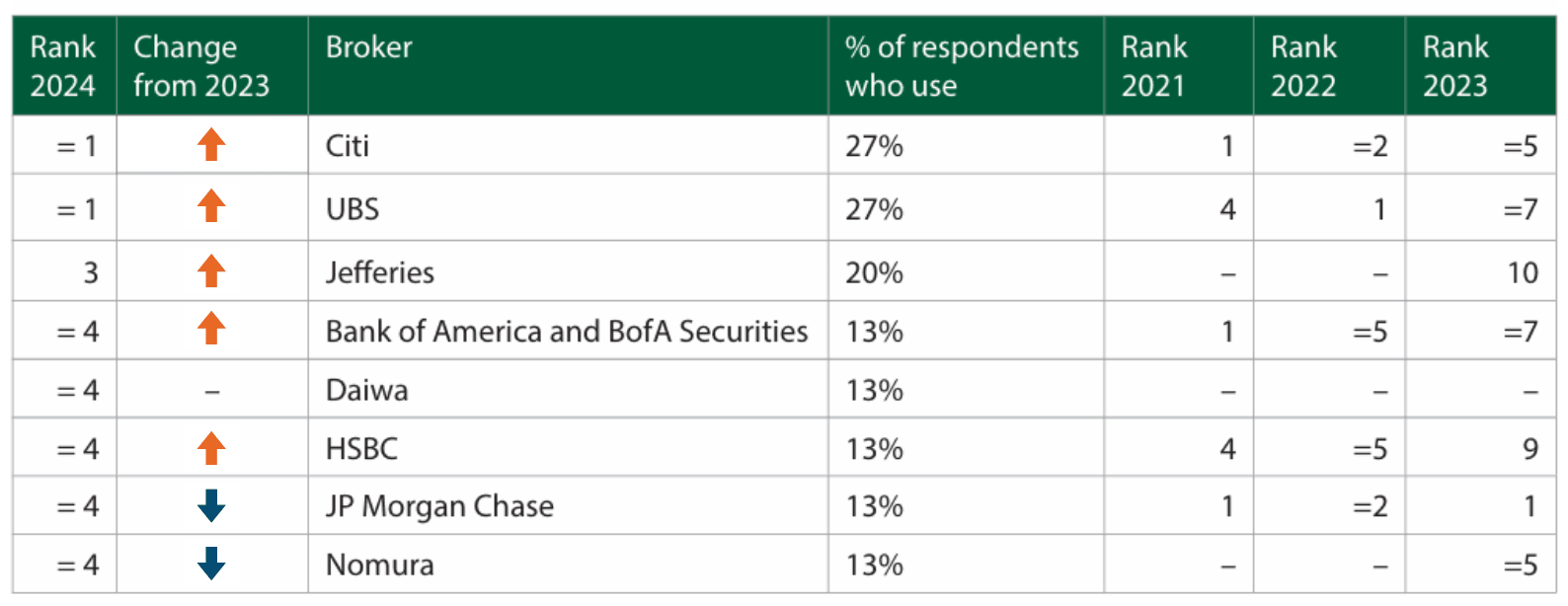

There’s a new first-choice broker for in-person roadshows this year, as Bank of America and Bank of America Securities move up one spot to take top billing after being used by 23 percent of respondents in 2024

Montreal, Denver and Dallas have all appeared as new entrants in the top destinations for IROs planning global roadshows, while New York, London and Toronto remain firm favorites

‘We have three strands to our roadshow program:

‘Post-results non-deal roadshows (NDRs): [We do these] four times a year. We still rely on brokers to organize these but will also provide target lists based on our database. Usually this consists of two days in Hong Kong and another one or two days in Singapore, together with a virtual NDR to cater to our US and EU investors. Senior management (often our CFO) usually attends these meetings, so we will primarily arrange in-person one-on-one meetings.‘Investor forums and conferences: We select some of the key forums to attend and prioritize the ones with great turnout. We usually sign up for one or two days, depending on the location (Hong Kong, Singapore, Shenzhen, Shanghai or Beijing) and investor interest, and may stay for an additional half-day or full day to conduct an NDR if demand is high.

'Our major shareholders are based in the US and UK, so we aim to visit them once a year. We will have brokers assist in arranging meetings and logistics, though most of the time we provide the target list.’

‘When I joined the company at the beginning of 2024, one of our goals was to be more proactive in our roadshow approach. What I wanted was to understand who we are dealing with in terms of partners and which investors we wanted to pursue strategically as a company – and then organize our roadshow or targeting efforts around those objectives. What became very clear is that even today, it’s still going to take me a bit of time to get there.‘We still spend more than half of our time with Canada-based investors, and the rest between the US and Europe plus a few in Australia. Within that, we spend around half the time with prospective investors and half the time with existing shareholders.‘Since I joined, we have been more actively doing competitive analysis: looking at our peers and their shareholder bases and understanding why they have better valuations than us. One element is that they’re spending more time outside of Canada, particularly in the US and Europe. We also spend around a third of our time equally with growth, value and yield investors, whereas our peers have a lot more growth-oriented investors in their base.'

Olivia Wang, IR director, Yue Yuen Industrial

‘While we all enjoy virtual because you can wear sweatshirts, at the end of the day, there’s great value to being in-person. We all realize that and I think companies do too.‘In-person events just help to build the relationship. The investment business is a very people business. We like to think that it’s all numbers and trends and data and so forth, but it’s not. It's a very personal business and it’s hard to develop that via the internet.’

In a year where access to capital is going to be more vital than ever, it’s fitting that an even higher proportion of companies have held roadshows: in 2024, 86 percent of companies across the globe embarked on an investor roadshow compared to 84 percent recorded in 2023’s research. This increase is consistent across North America and Europe but not in Asia, where there has been a 2-percentage-point drop in the proportion of firms going on roadshows year-on-year. Although this could look like a bucking of the trend, it is instead perhaps a reversion to the mean after a significant increase from 2022 to 2023 (54 percent to 76 percent).

Mega-cap companies remain the most likely of any cap size to embark on a roadshow and small caps the least likely. Compared to the year prior, however, mega-caps are slightly less likely and small caps slightly more likely to do so. This perhaps represents an added need for smaller companies to get out into the market in order to attract appropriate investors, compared to their larger peers.

The average number of roadshows carried out by IR teams has fallen slightly year-on-year, from 6.1 in 2023’s report to an average of 5.8 in 2024. This is driven by the average Asian team dropping 1.6 roadshows from their schedules, perhaps reflecting shrinking budgets or a focus on existing shareholders for companies in this region. This reduction is also driven by mega-cap companies, who went on more than two fewer roadshows on average in 2024 than they did in the year prior.

‘I’ve come to appreciate that the IR business is a lot like prospecting: you always need to be meeting new investors and always trying to go after new business.‘This year, we’ve been more discerning, turning down offers from brokers for meetings because we want to be more selective about who we put our management team in front of. We’re working with a new IR service partner to undertake global targeting analysis to be able to help us with this and come up with a list of – for example – growth-oriented investors who are interested in our peers, our sector, to come up with a target list. Going into 2025, I’m hoping to flip our shareholder base around and spend a lot more time with prospective shareholders in new markets externally.‘The next question is who is going to help me with that, however, as it seems like, at least for some markets, you need to go through a broker or at least a private sales desk, which can be expensive. I’m still wondering how I’m actually going to reach out and get meetings with these people.’

Overall, the figures show that IROs are resoundingly embracing in-person roadshows as their preferred method of meeting new investors, with the proportion of respondents saying they only rely on virtual events falling to just 4 percent in 2024, down from 8 percent in the year prior. The trend of virtual roadshows – which became so popular during the pandemic – has certainly become part of most IR teams’ toolkit today. However, as was the case in 2023, around a half of all IR teams conduct both in-person and virtual roadshows on an annual basis, as they blend bespoke events for local and overseas investors as best fits them.

The high proportion of teams only conducting in-person roadshows has been driven by respondents in North America and at mega-cap companies. Almost two in five (39 percent) IROs in North America only held in-person roadshows in 2024 – compared to 29 percent of the region’s IR teams the year prior – while 45 percent of mega-cap respondents did the same, a notable jump from 19 percent in 2023.

As readers may anticipate, respondents in Asia (5 percent) and at small-cap companies (9 percent) are the most likely to only have held virtual roadshows in 2024, given the likelihood that the former are further away from key investors and that the latter have a smaller budget for travelling internationally. Both figures are significantly lower in 2024’s results than the year prior, however, indicating that even for these companies, in-person roadshow events are still preferred.

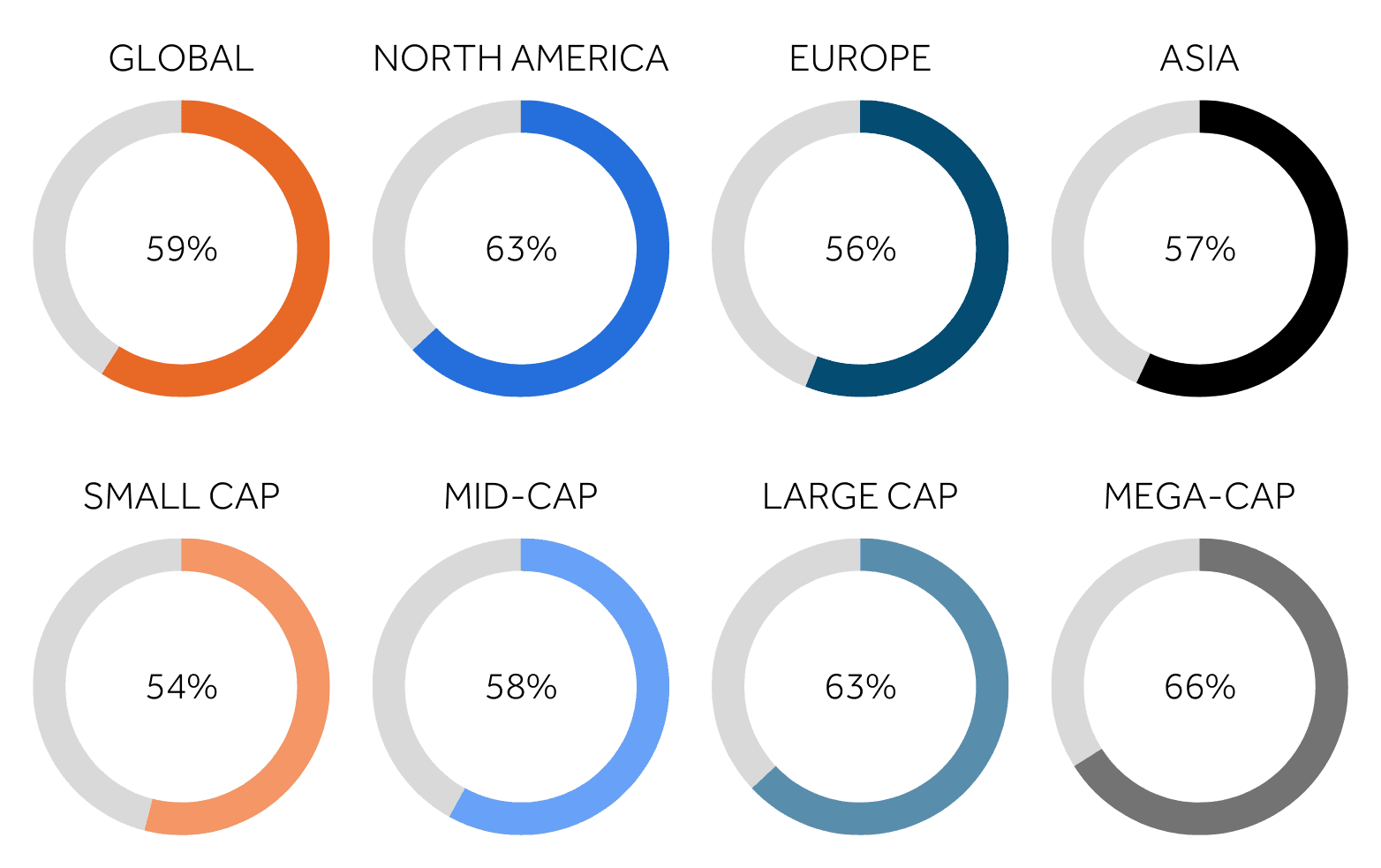

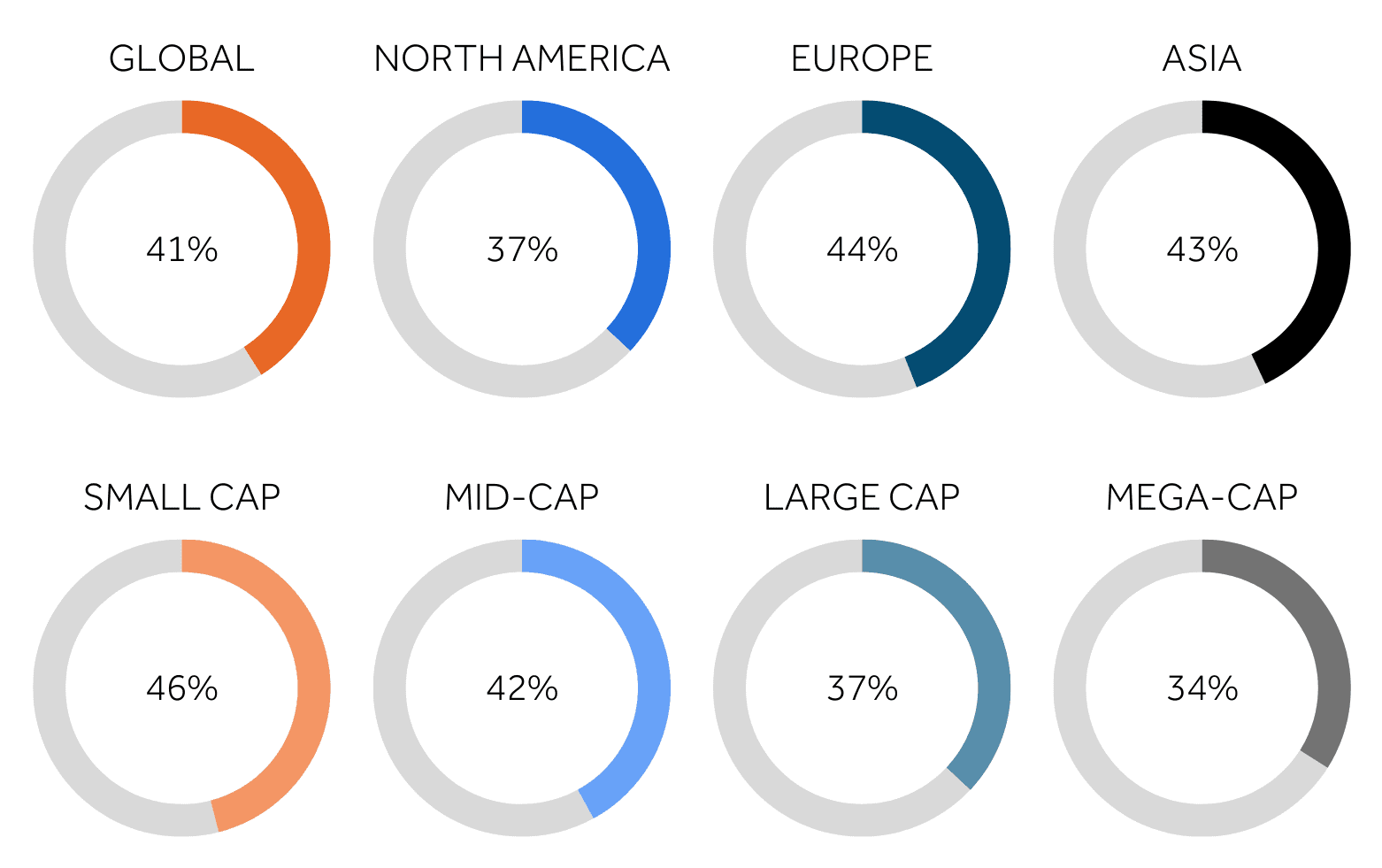

The overall proportion of respondents who have embarked on a roadshow in the past 12 months continued to grow year-on-year, with almost three in five (59 percent) doing so on a global basis. This increase is largely universal but was particularly driven by a higher proportion of firms in North American and mega-cap respondents saying they went on roadshows in 2024.

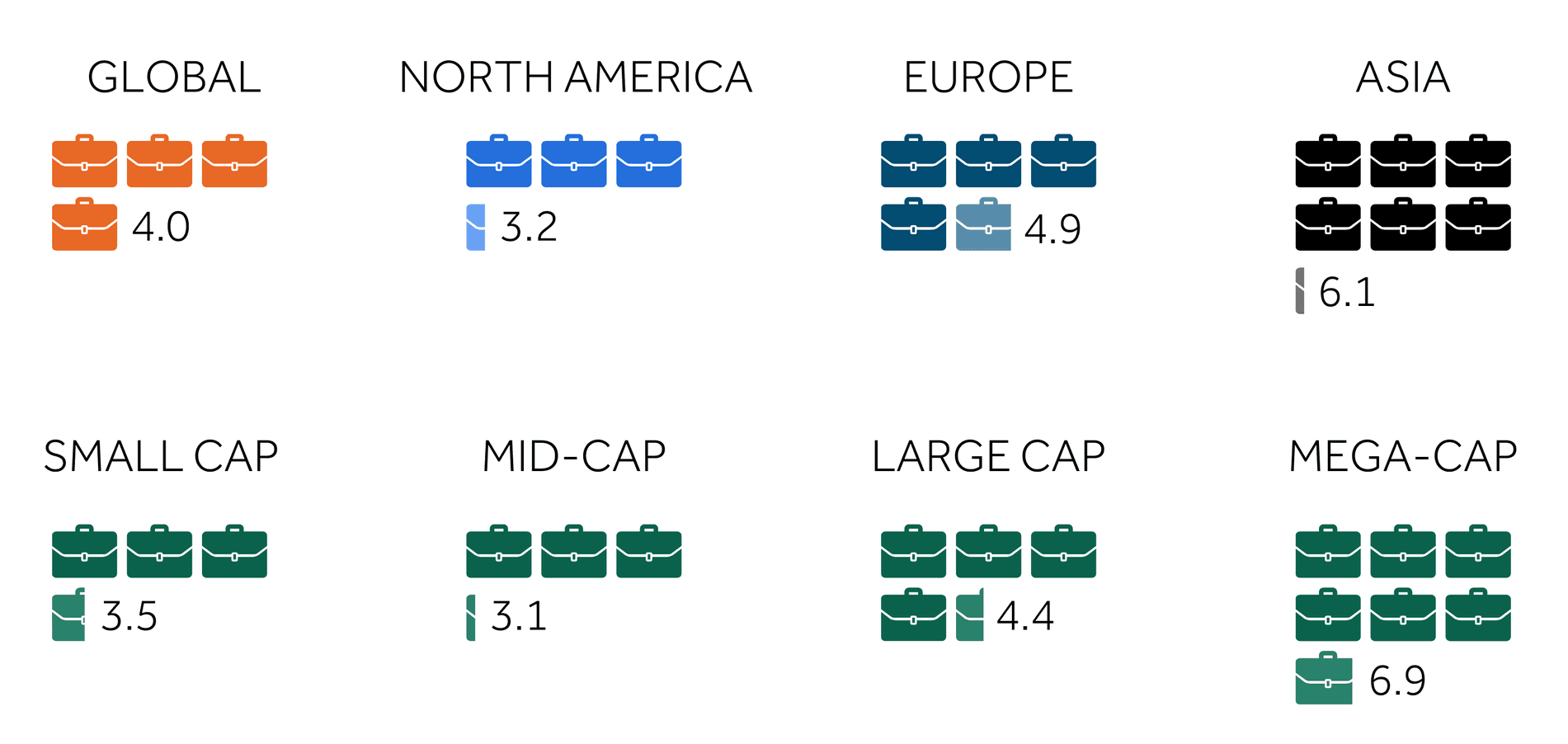

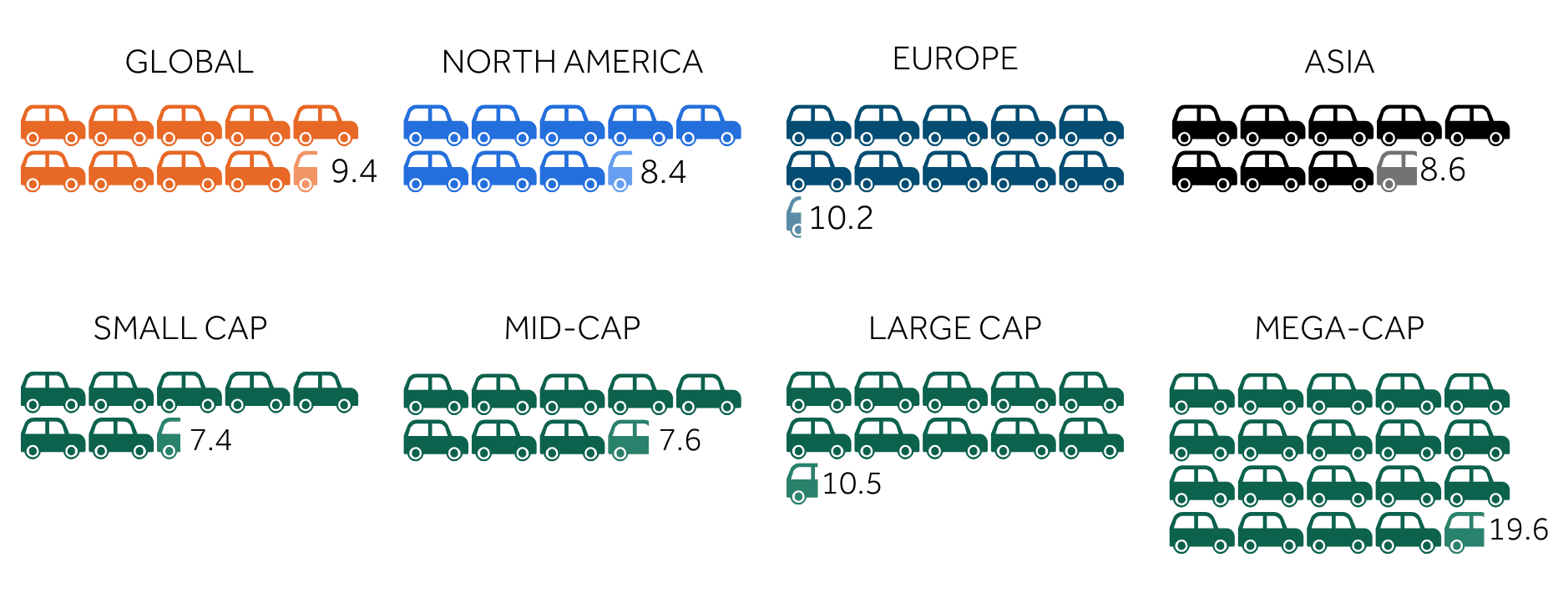

Interestingly, companies tended to keep their roadshows more focused in terms of time spent on the road in 2024. The average number of days spent travelling for roadshows decreased by 1.4 days year-on-year, with Asian companies slimming down their schedules by a notable average of 3.8 days. When split by cap size, only mega-cap companies spent more time travelling for roadshows in 2024 (19.6) than in 2023 (18.8).

All this may reflect the added budgetary pressure that most IR teams found themselves in during 2024, prompting them to focus their roadshow efforts in as short a time as possible.

The average number of in-person roadshows that IR teams organized has also ticked up year-on-year, with the average team going on 0.4 more in the past 12 months than in 2023. This increase is particularly pronounced among Asian respondents, who added 2.5 roadshows to their calendars year-on-year across 2024, presumably as the last remnants of Covid-19 restrictions on travel were lifted in the region. The average company of each cap size expanded their roadshow calendars in the past 12 months, too.

There is a corresponding drop in the proportion of companies going on virtual roadshows in 2024 to the increase in those going on in-person roadshows (2 percentage points), with the virtual format falling in popularity most among North American respondents (a 6-percentage-point drop year-on-year) and mega-cap respondents (12 percentage points down).

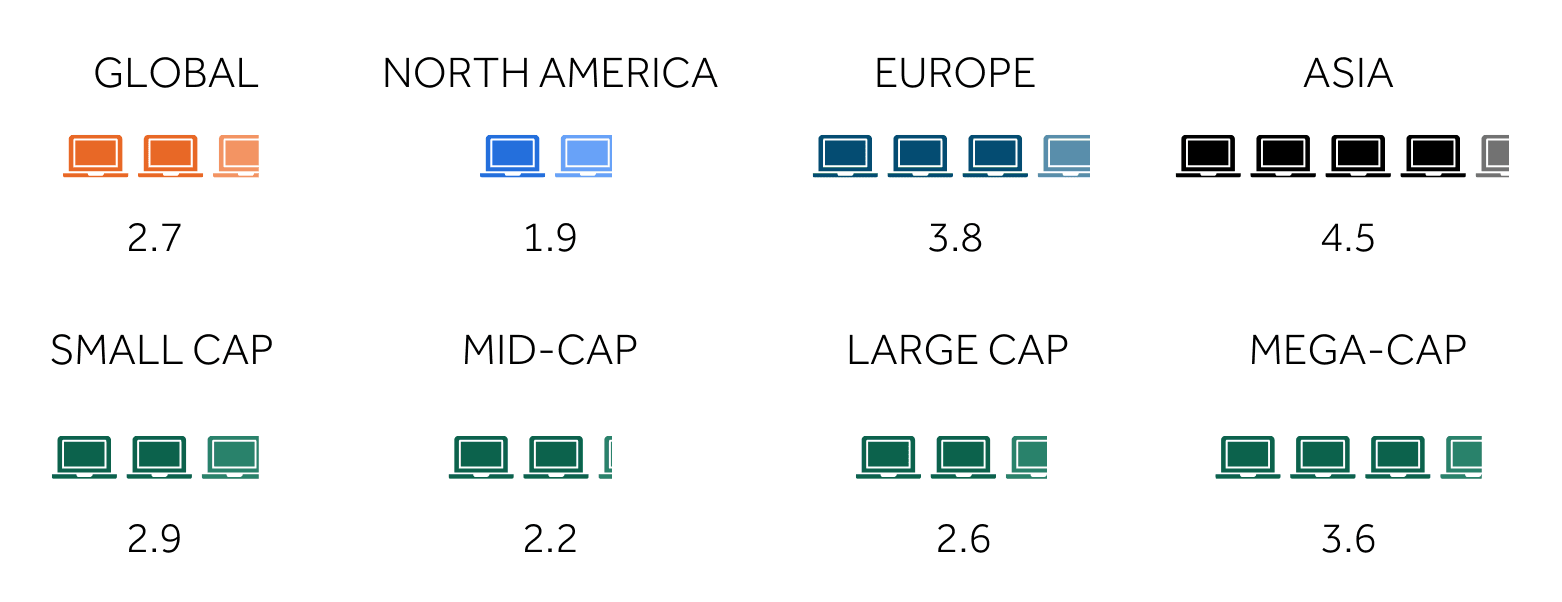

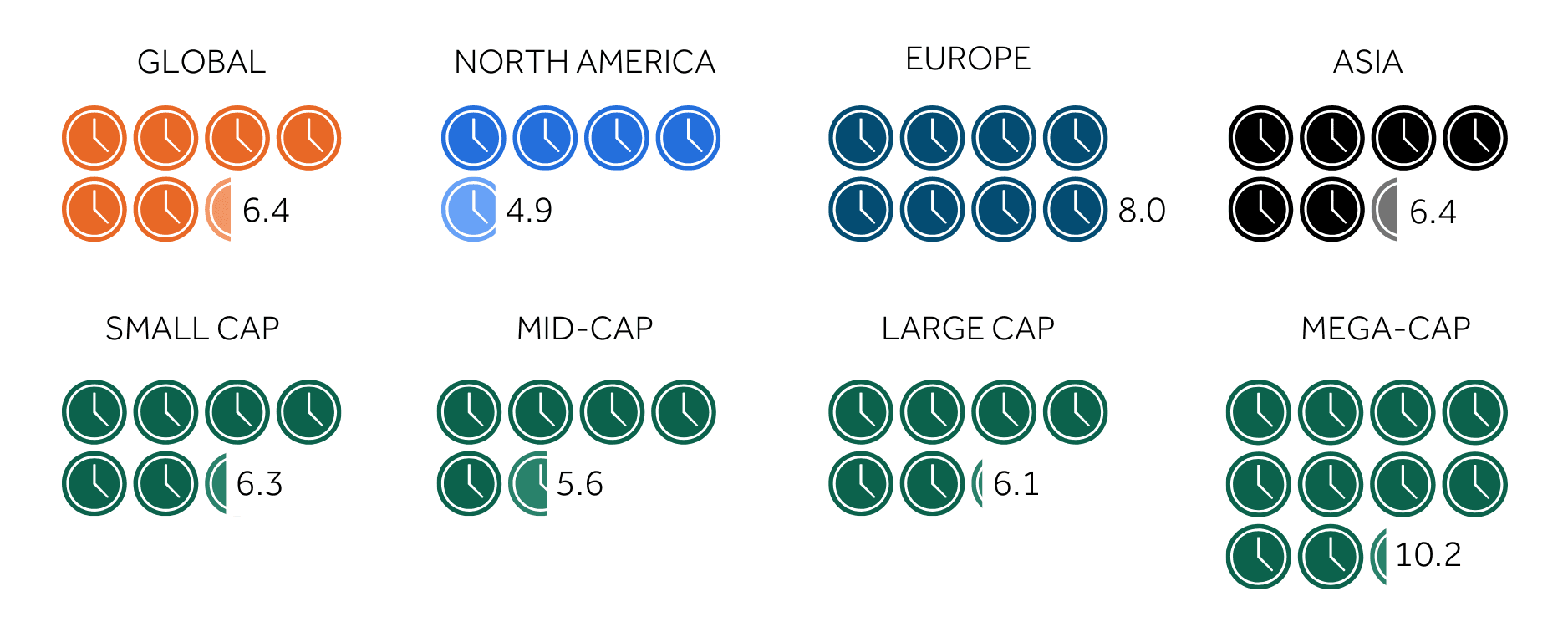

As may logically follow, both the average number of virtual roadshows embarked upon and the average number of days spent on virtual roadshows have fallen year-on-year. While Asian respondents still go on the most virtual roadshows of any region, this number has almost halved since our previous report (from eight roadshows to 4.5 this year). European firms spend the most time on their virtual roadshows (eight days).

Similarly, mega-cap companies have both reduced the number of virtual roadshows they went on (2.4 fewer virtual roadshows) and have shaved the most time off of their virtual roadshow calendars (losing 2.8 days on average) year-on-year.

‘We do both virtual and in-person meetings, with a mix of conferences and non-deal roadshows. The latter are mostly broker-led but also mix virtual and in-person so that we can cover more locations and more prospective investors. Typically, our roadshows will be two days long, taking in two cities, but sometimes we just do a one-day trip to one city. When we go to conferences, it could extend to three days with an extra day of meetings tacked on. It’s rare for us to spend longer than that. ‘I’ve already asked myself whether we want to extend beyond three days next year if we look more at the US and Europe. However, if I’m taking my CEO to New York, I may as well go to Boston, too, or if I’m heading down the West Coast I may as well take in multiple cities because it’s a long way to go. Maybe at some point our sweet spot will be closer to three days.’

‘We preferred virtual roadshows during the pandemic due to health and safety concerns. Since the second half of 2023, our preference has gradually shifted back to in-person meetings. However, the demand for virtual meetings remains strong. For example, overseas investors can easily connect with us through virtual meetings. Some investors or analysts still prefer virtual meetings, especially for group calls or panels.’

After getting significant management buy-in for roadshows of all types in 2023, IROs maintained a similar level of support from their C-suite across 2024 though there were some slight drop offs. The total proportion of in-person roadshows that had no management attending grew by a small amount (up 3 percentage points to 22 percent) and the total proportion of such events that had a CEO, CFO or both management figures attend fell by the same rate (down 3 percentage points to 68 percent).

While this can be seen as management having reached its peak on the time available to IR, it could also be indicative of increased confidence in IR to manage more of those interactions independently – and of investors perhaps enjoying greater confidence after the post-pandemic years and increased volatility that might have required more C-suite reassurance.

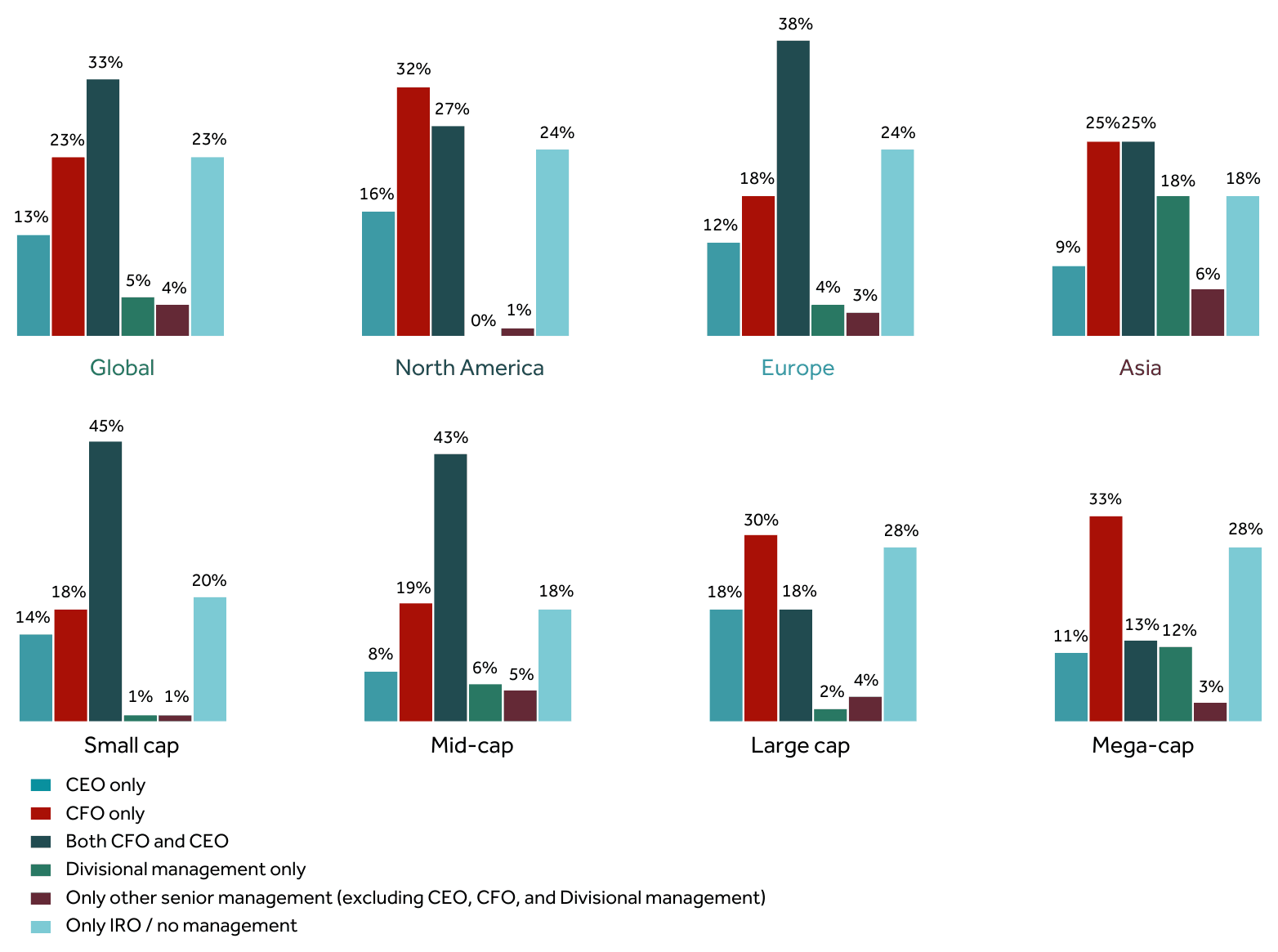

For virtual roadshows, average management attendance remained broadly consistent, but a higher proportion of such events had both the CFO and CEO attend (up 10 percentage points year-on-year). This implies that, as roadshow calendars have stabilized, so too has the level of support that management teams are willing or able to give IROs for them.

When examined by region, a few outliers emerge. For one, European IROs are the least well-served by their management team for in-person roadshows, with 31 percent of such events only attended by the IRO themselves. For virtual events, North American IROs have gone from having just 5 percent of roadshows with no management representation up to 24 percent IRO-only events in 2024.

When it comes to company size, respondents report a return to the trend observed in previous years: the likelihood that an IRO can count on their management team to attend an in-person roadshow decreases as cap size increases, with the trend slightly less predictable for virtual roadshows. This reflects the likelihood that management attendance is even more crucial to smaller companies, who rely more on individual shareholders, rather than mega-caps who are likely to have many more investors to put their C-suite in front of in a given year.

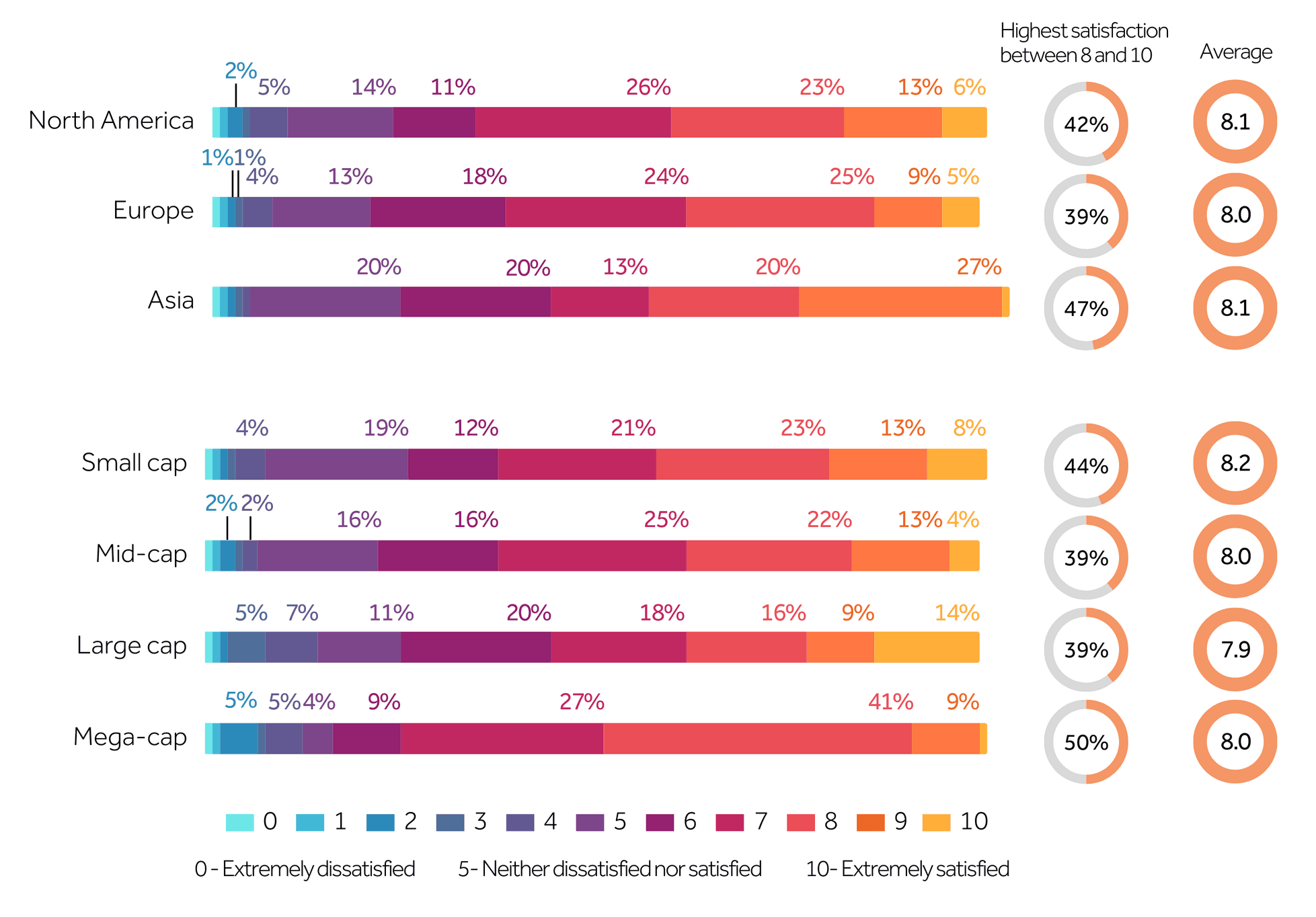

As the roadshow landscape appears to be stabilizing, so too are IROs’ broad levels of satisfaction with the format. Matching the findings from our 2023 research, 72 percent of all those polled rated their satisfaction with in-person roadshows at between eight to 10 out of 10, while the average rating given by IROs around the world came out very slightly up on 2023 (9.1 from 9 out of 10).

Meanwhile, there has been a slight dip in overall satisfaction with virtual roadshows year-on-year, with 42 percent of respondents scoring their satisfaction with the format at least eight out of 10. The average rating of 8.1 has remained exactly the same year-on-year, however.

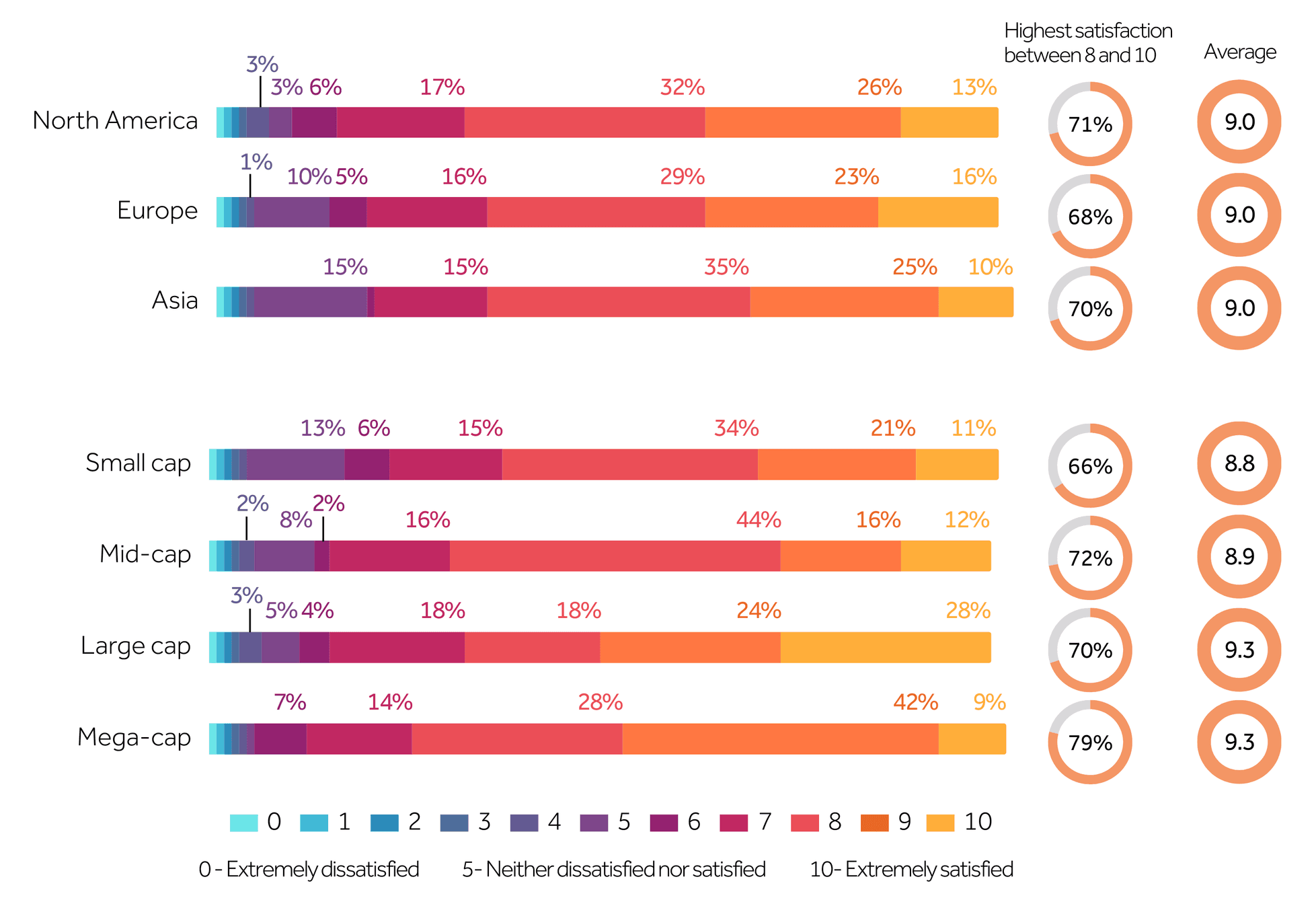

Those sentiments have become nearly uniform across regions over the past year, though when split by cap size, figures show that small-cap firms are generally less satisfied than average with in-person roadshows and more satisfied than average with virtual roadshows.

‘We are satisfied with our recent roadshows. Overall, if an experienced analyst with solid knowledge of the company and industry accompanies the roadshow, it would enable IR to communicate more efficiently and in greater depth with investors.’

‘In 2024, my satisfaction with our IR targeting was only six out of 10, but I’m hoping we can take that to an eight or nine in 2025. It’s not only about quantity – we’re going to finish the year with 10 roadshows and that feels like a good number, averaging at about one a month. In terms of quality though, I’m not happy with them, because we’re not spending enough time with potential future investors and exploring new markets.'‘What I am happy with is that since I joined in January 2024, and because of the changes we’ve carried out internally, we’re spending more time with investors without our management team. Maybe at the beginning of the year we were spending 10 percent of our investor engagements without management, and now we’re up to about 25 percent with just the IR team. That’s because we’ve built relationships and trust with those investors, so I’m happy about that.'

‘I’m not happy with the fact that I still can’t always meet the investors we want to meet with. Brokers sometimes put me in front of their clients and not the ones I want to target, which is why my satisfaction is only at six out of 10. If I can get to the point in 2025 where I have the same number of roadshows but in a bigger variety of cities with more new business, I’d be more satisfied.’

‘I believe that if an analyst says that a meeting was not worthwhile, that is the analyst’s fault. It’s not the company’s fault but we frequently blame companies.‘The bottom line is we’ll do whatever [the IRO] asks. And if you do a good job, get them in front of the right people and the day goes well, they’re going to remember that and appreciate that. Then, next year, maybe they’ll come back. It should be well-planned, well-orchestrated, we should keep them on time and their meetings should be productive. If you check all those boxes, then your odds of having another roadshow go up.’

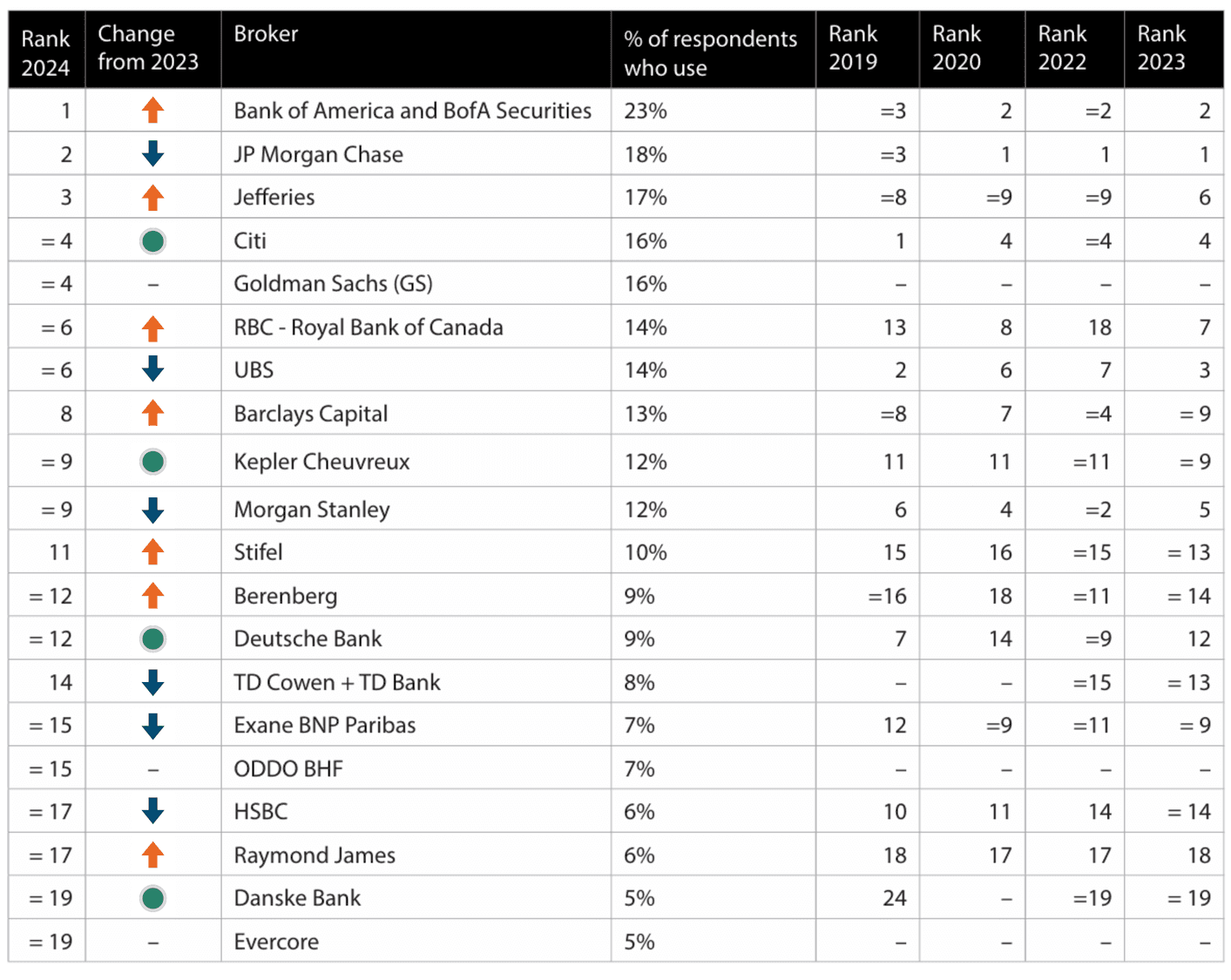

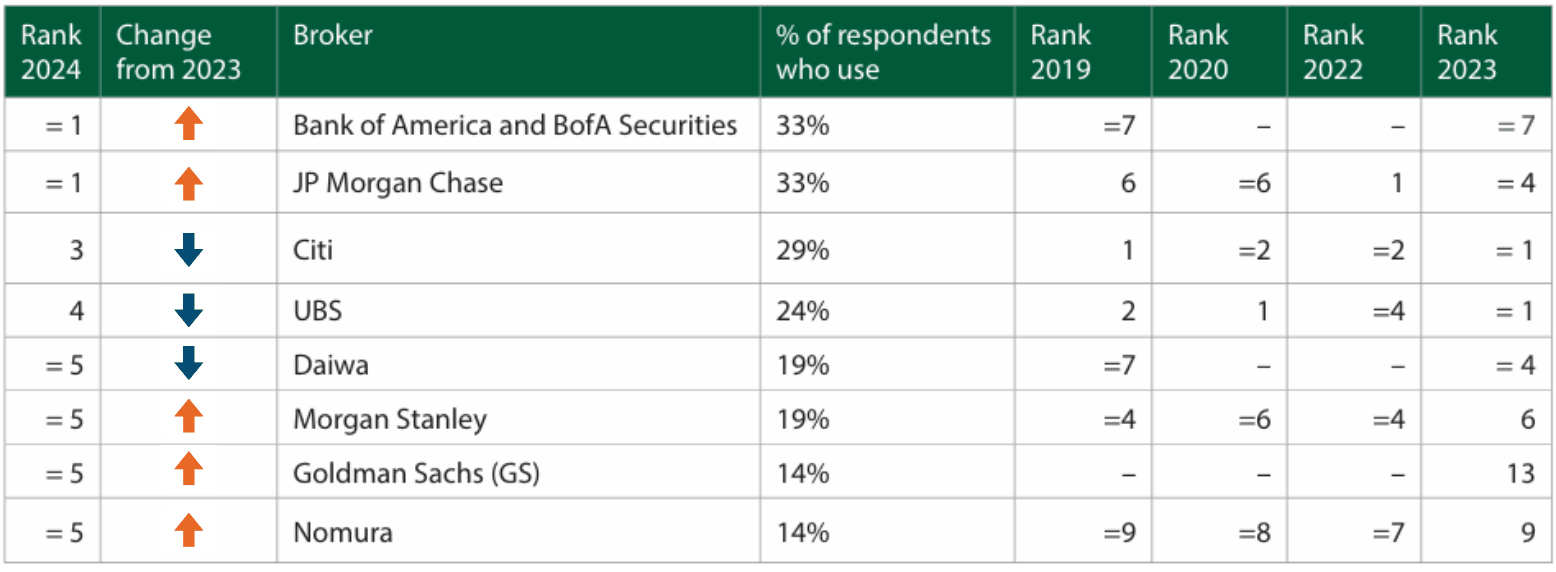

There’s a new first-choice broker for in-person roadshows this year, as Bank of America and Bank of America Securities move up one spot to take top billing after being used by 23 percent of respondents in 2024. JP Morgan Chase, 2023’s top-ranking broker, falls one place to second spot, followed by Jefferies (up three places year-on-year), Citi (maintaining its fourth place) and Goldman Sachs (a new entrant to the top 20 this year). Both Bank of America and JPMorgan Chase have retained their positions as the two most-preferred brokers every year since 2020.

Other improvers this year include RBC (up from seventh to joint-sixth), Barclays Capital (up from ninth to eighth) and Stifel (up from 13th to 11th). On the other hand, UBS has slipped from third in 2023 to sixth-favorite in this year’s rankings, while Morgan Stanley, TD Cowen + TD Bank and Exane BNP Paribas have all also fallen for in-person roadshows.

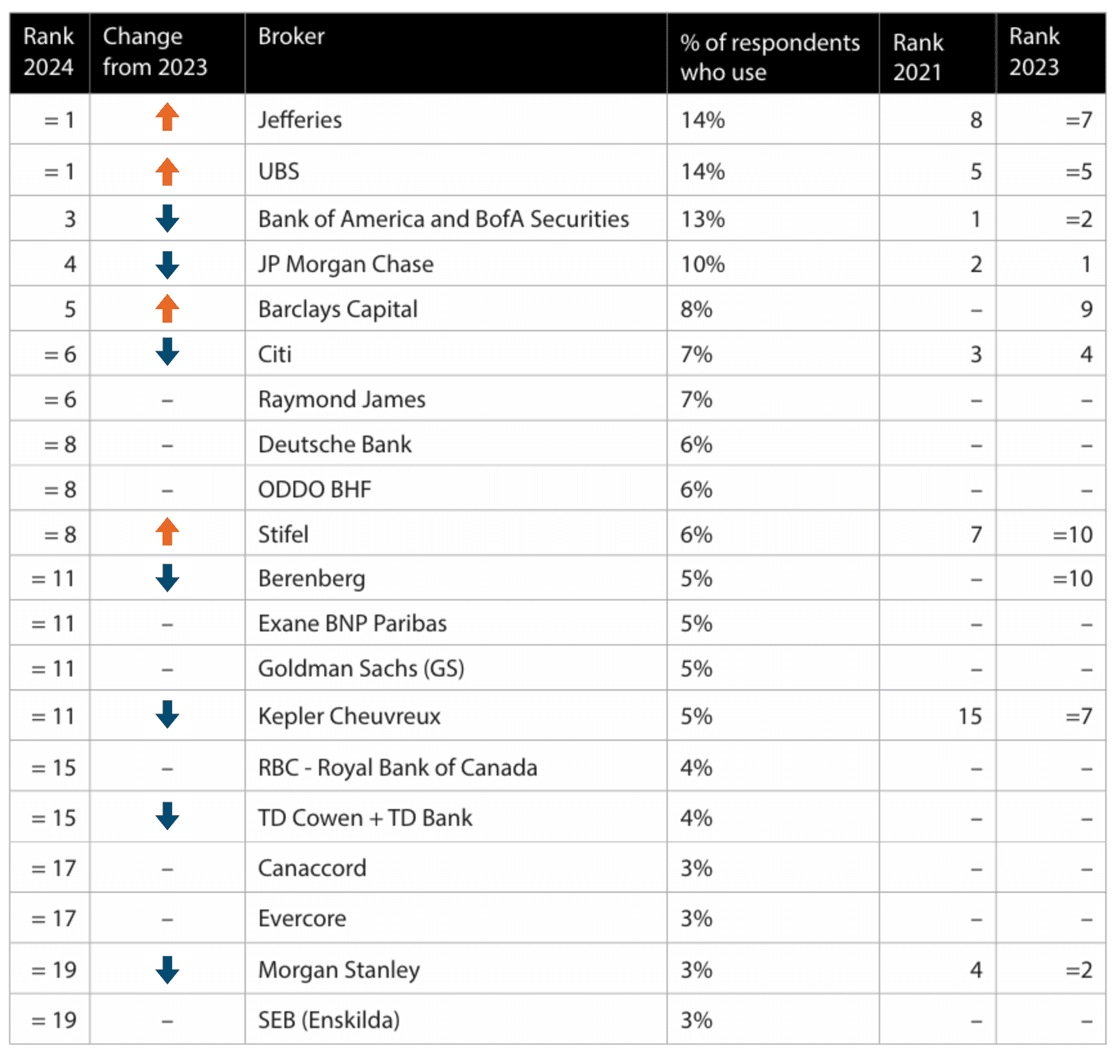

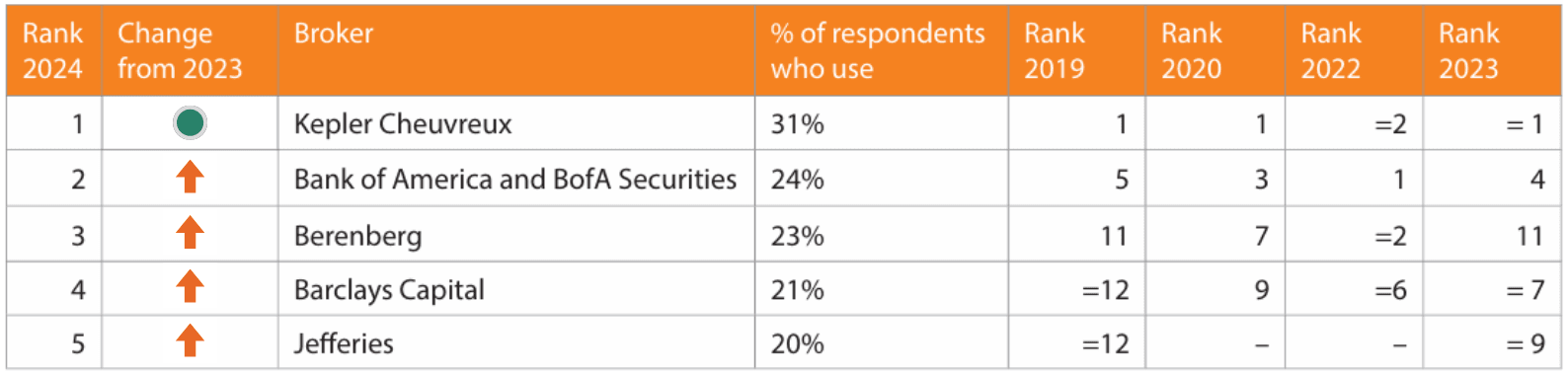

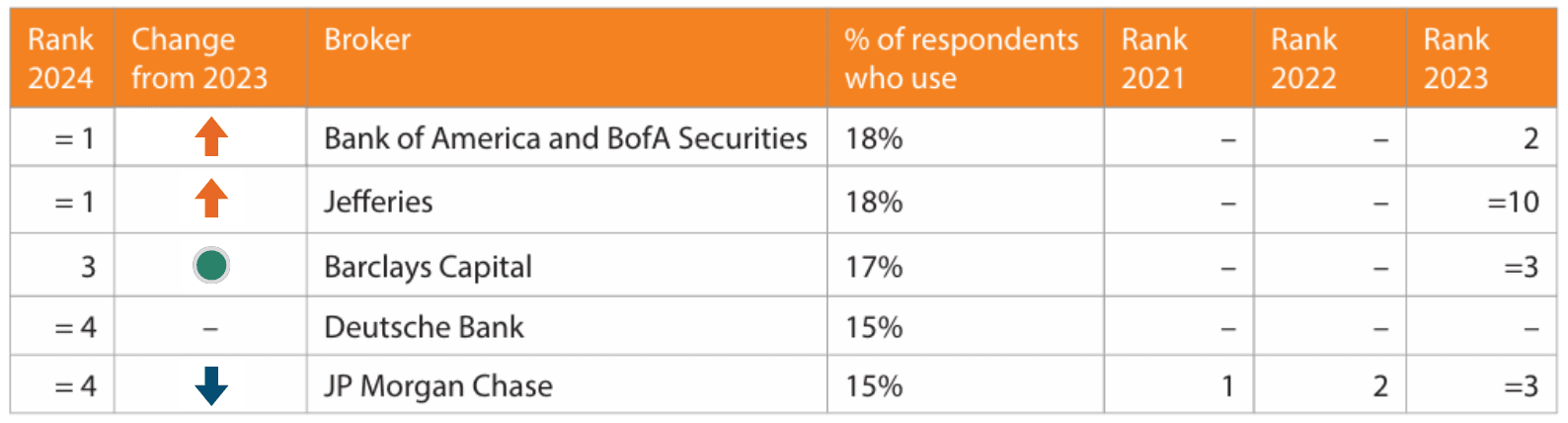

There is significantly more change in the rankings for the most-used brokers for virtual roadshows, with Jefferies and UBS sharing the top spot after ranking seventh and fifth respectively in 2023’s rankings. That year’s number one – JP Morgan Chase – has dropped down to fourth spot in 2024, while Bank of America and Bank of America Securities, and Morgan Stanley, who held joint second place in 2023 are down to third and equal 19th position in 2024, respectively.

There are several new entries in the top 10 brokers for virtual roadshows this year: Raymond James, Deutsche Bank and ODDO BHF all appear at the top of the ranking for the first time in several years.

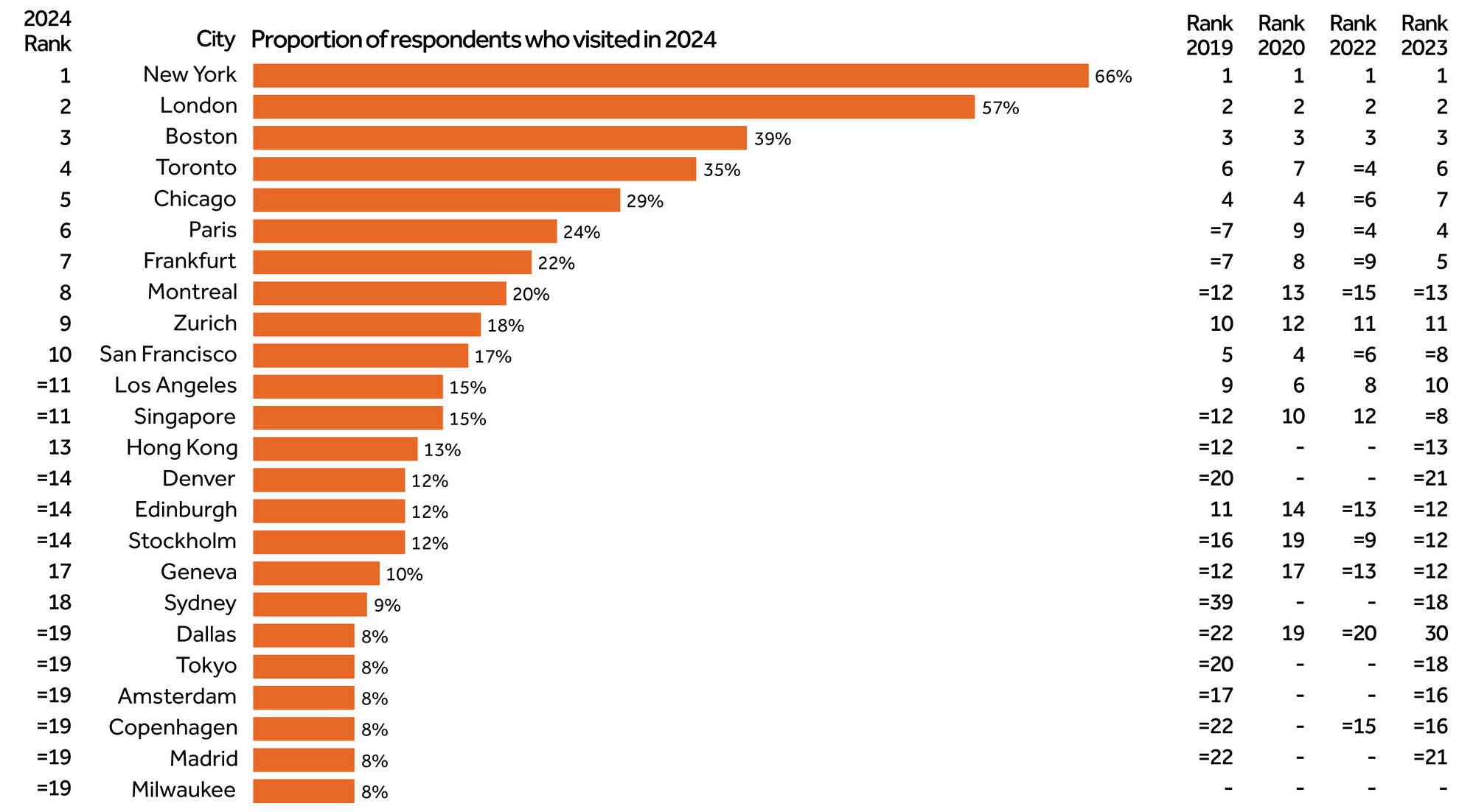

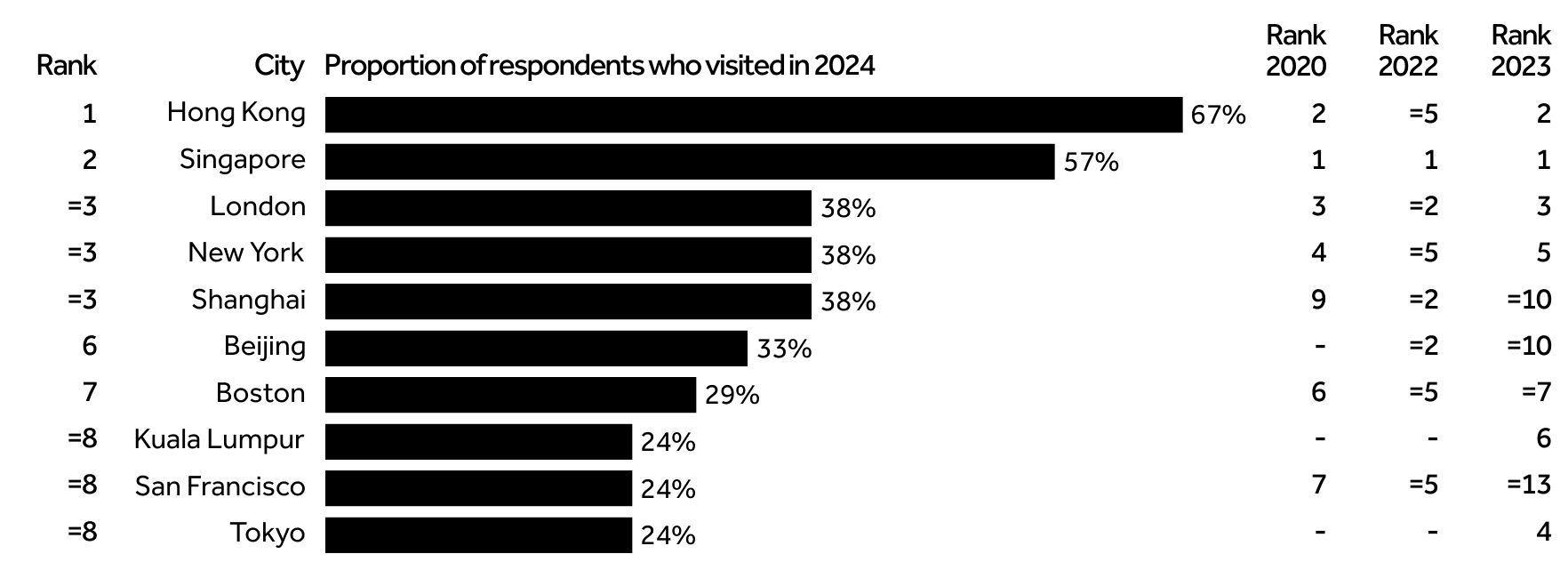

The top three roadshow destinations have remained unchanged since before the pandemic, with New York, London and Boston remaining the most popular cities to visit for IROs. Both American cities have increased in popularity year-on-year, with two-thirds of IROs polled (66 percent) taking their roadshow to the Big Apple in 2024. These three cities were regularly the top three most-visited cities for in-person roadshows even before Covid-19 prevented IR teams from travelling to see their investors.

Several cities are emerging as increasingly popular destinations for IR teams in 2024, however: Montreal, which has nearly doubled in popularity year-on-year (11 percent of IR teams visited here in 2023, versus 20 percent in 2024), is the single biggest mover, but Denver (up from 21st to 14th) and Dallas (up from 30th to 19th) have both emerged as new options. Perhaps the planned Texas Stock Exchange, first announced in September 2024, may capitalize on the popularity of Dallas as a roadshow destination. Elsewhere in the US, Milwaukee has emerged as the only new entrant into the top 20 most popular cities, with 8 percent of IR teams saying they visited the Wisconsin city last year.

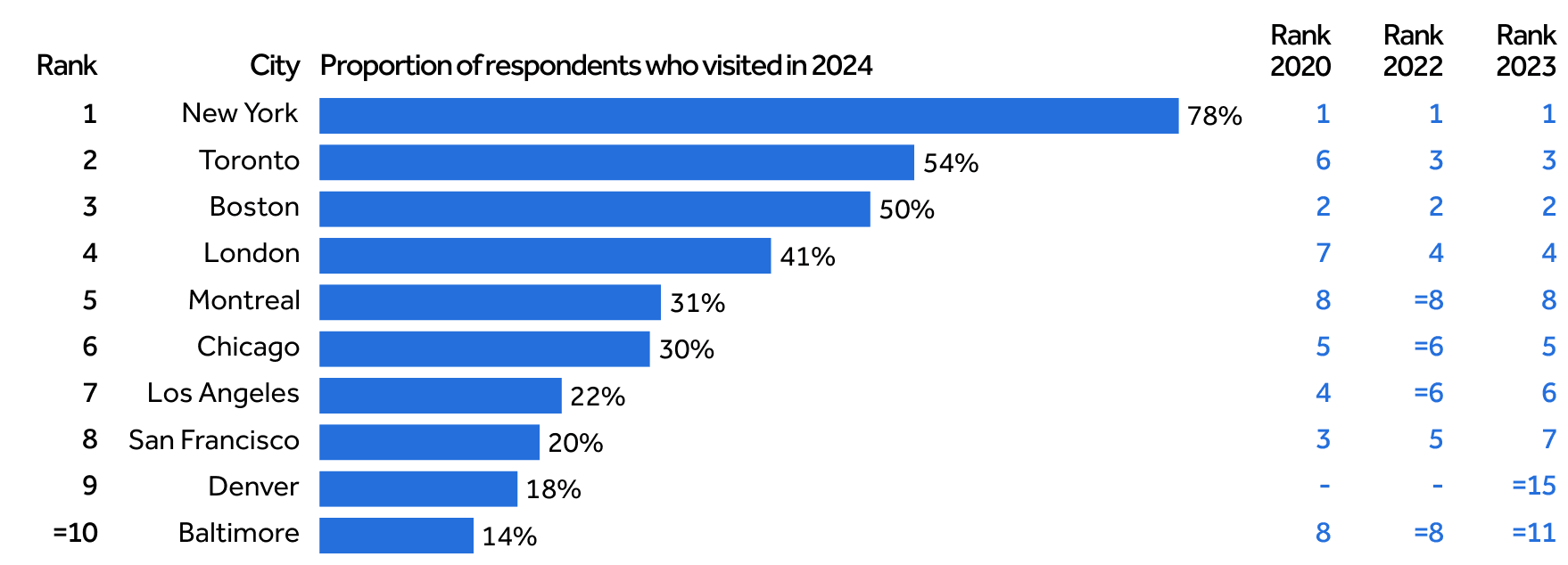

When broken down by region, respondents show similar city favorites as seen in our 2023 research. For North American IROs, New York, Toronto and Boston remain the most popular destinations, though Toronto has taken over the number two spot. Meanwhile, Montreal has climbed up the rankings into fifth spot as Vancouver, the ninth most-popular destination in 2023, slipped down to joint 10th spot this year.

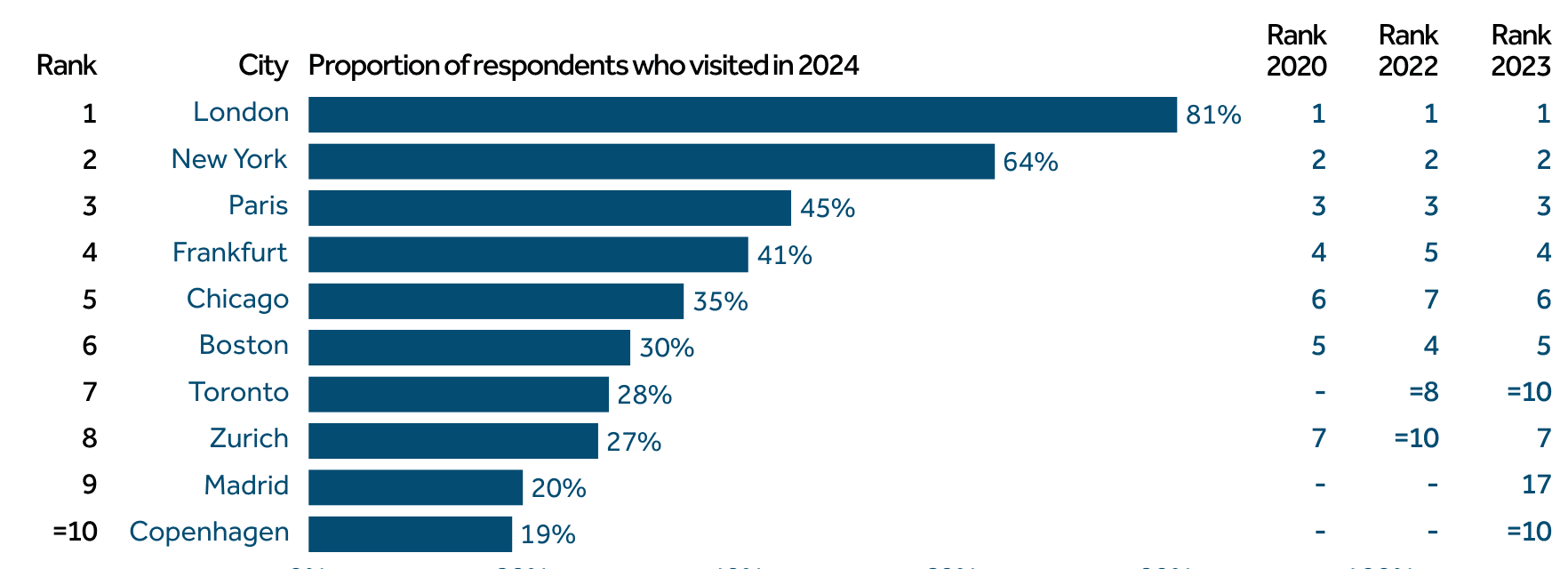

In Europe the top four destinations remain unchanged from 2023. Again though, Toronto has become an increasing part of IROs’ plans, visited by 28 percent of respondents from the continent in 2024. Madrid has also climbed the rankings, after one in five IROs in Europe said it formed part of their roadshow plans over the past 12 months. The proportion of European IROs visiting New York has grown by 9 percentage points year-on-year, with nearly two-thirds (64 percent) travelling there in 2024.

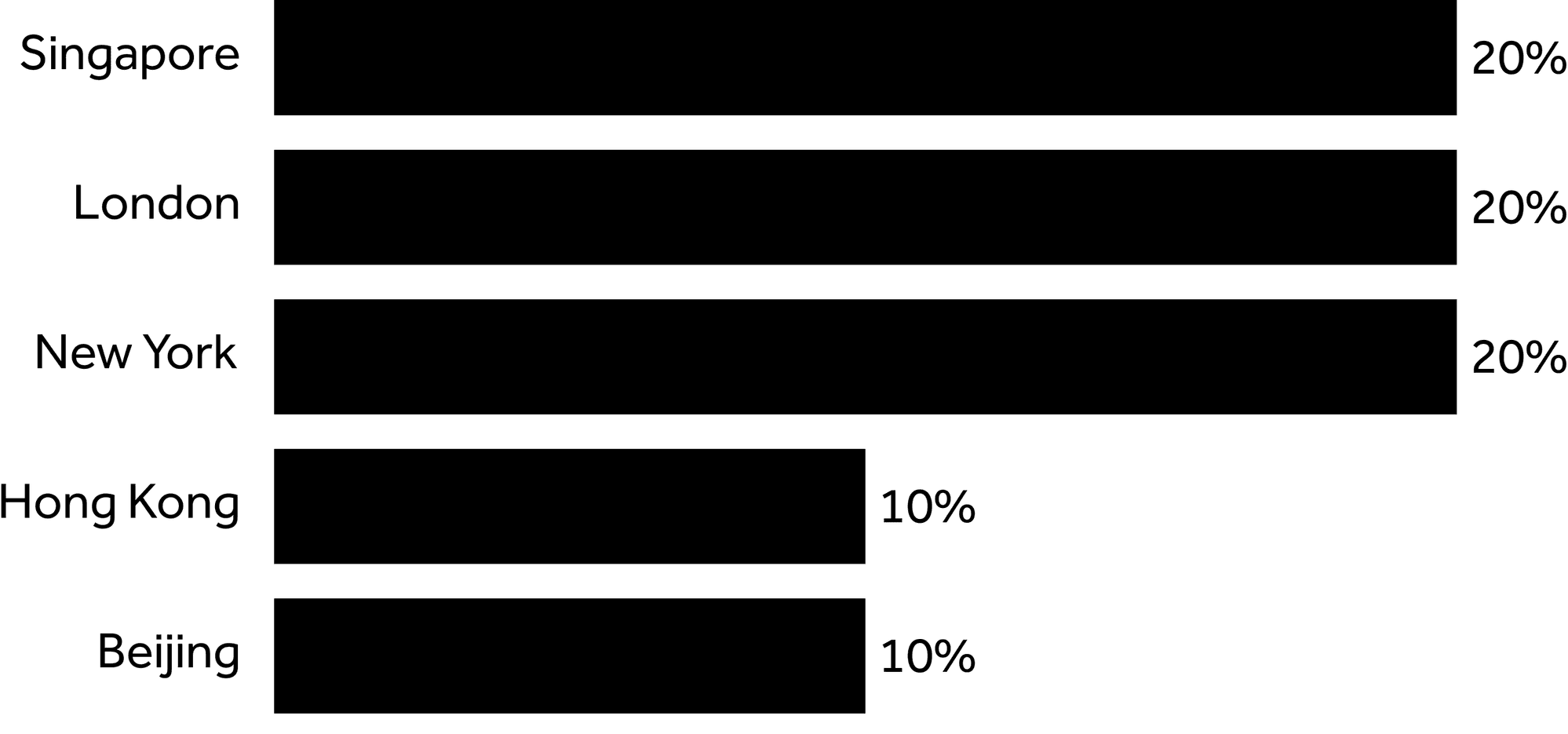

For Asian respondents, Hong Kong has outstripped Singapore as the most popular destination with more than two-thirds (67 percent) of IROs visiting the city. Now free of any lockdown restrictions, Shanghai has returned to near the top of the table, rising from 10th place in 2023 to its equal-third ranking in 2024.

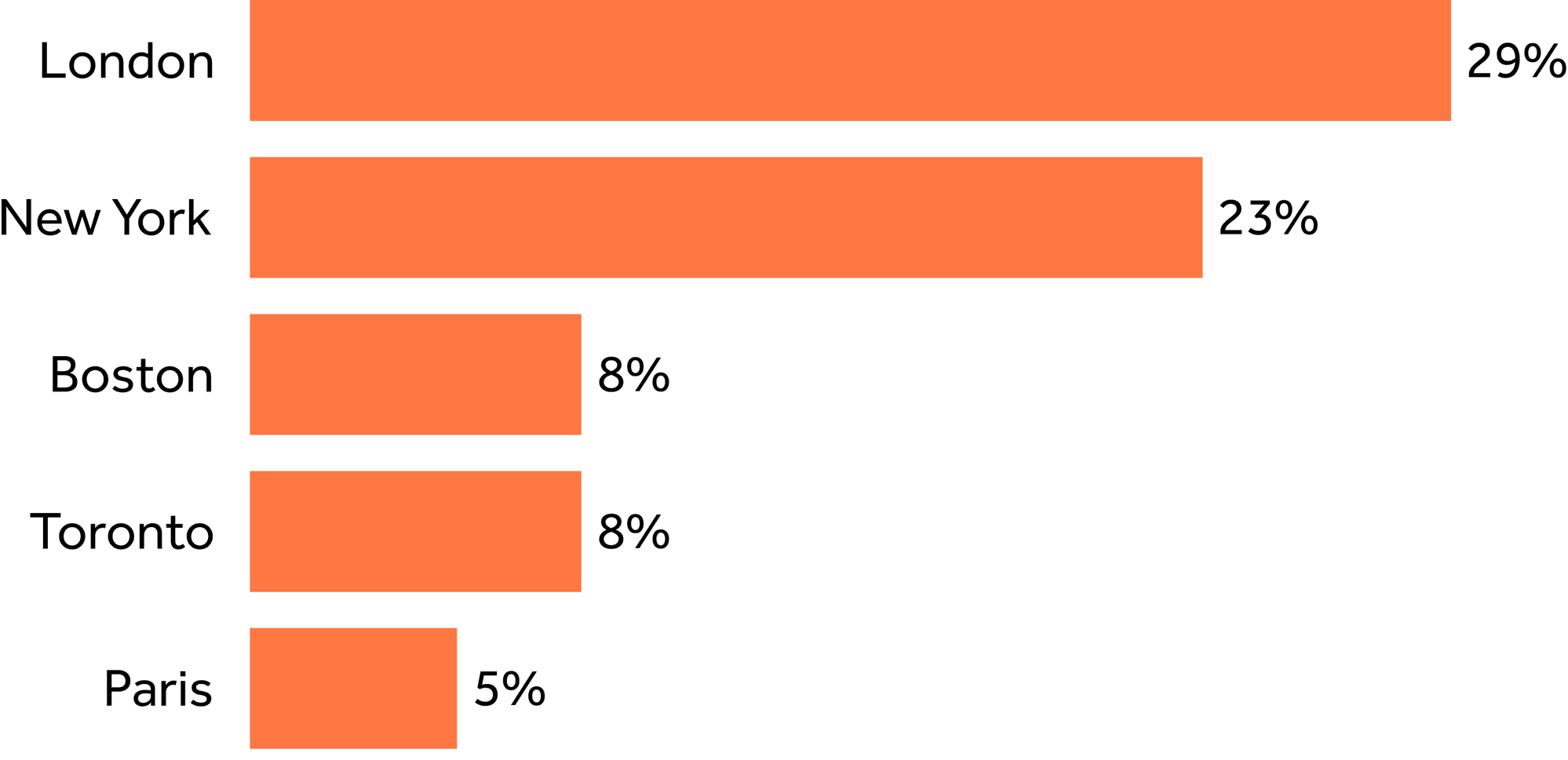

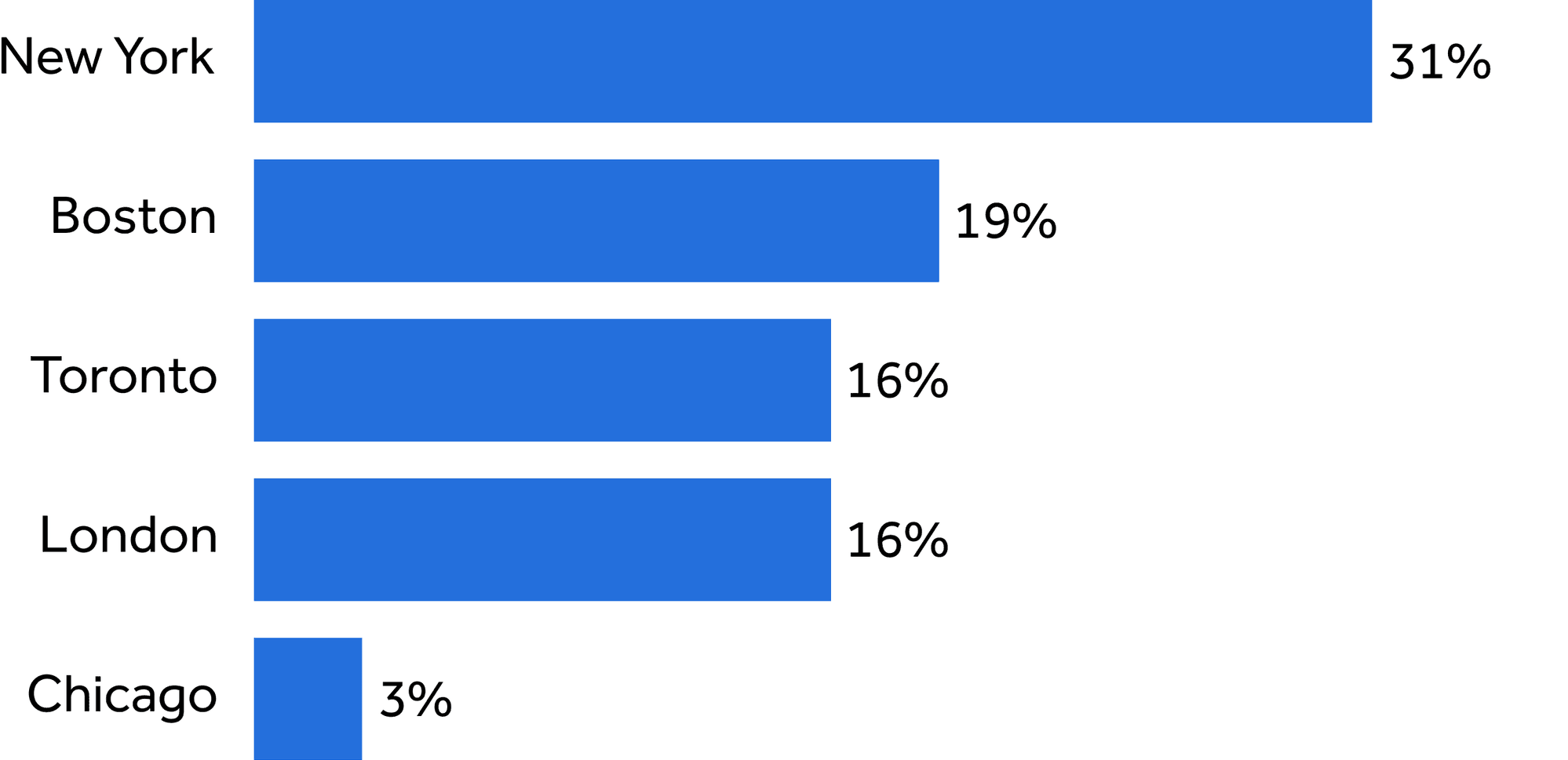

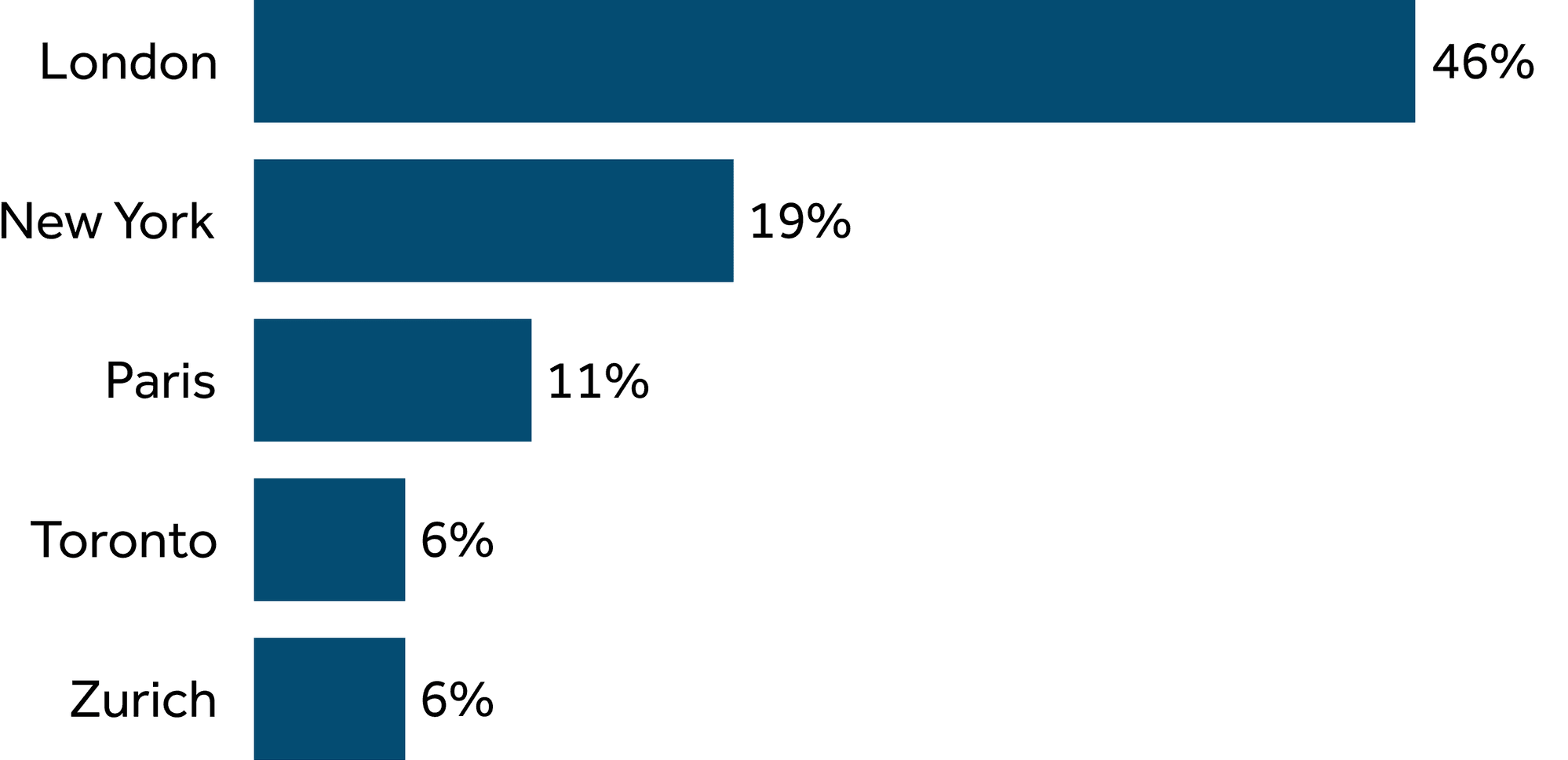

When IR professionals were asked to pick their favorite city destination for in-person roadshows, London retained its badge as the number one choice, with 29 percent of respondents picking it as their top option, and 46 percent of European IROs saying the same. Similarly, North Americans remained loyal to New York, with 31 percent of IROs in the region naming it their favorite. Boston, Toronto and Paris make up the rest of the top destinations globally after Singapore, the third-favorite city in 2023’s rankings, slipped down the table in 2024.

‘In the past two years, we have conducted roadshows in Hong Kong and Singapore, in Shenzhen, Shanghai and Beijing in mainland China. Also in New York, Boston, San Francisco and Santiago in the US, and in London in the UK. The Middle East was within consideration; it’s just that we haven’t started to go to this new destination yet.’

‘Today we spend a lot of time in Canada: in Montreal, Toronto and to a lesser extent Vancouver. In Europe, it’s quite London-centric and in the US it’s very New York-centric. If I think about what I would like to add, Sydney in Australia has a large group of investors there and is a large focus for us. In the US, we want to target Boston, Chicago and the West Coast, perhaps adding Washington too. In Europe, London will remain a focus because it’s a hub – that is the reality – but Paris, Oslo and maybe Geneva or Zurich would be high-priority locations for us in terms of the investor profiles we’re targeting.

‘Being completely objective, even if other regions are not a priority for us, I think there are pools of money that might fit the profile of investors we’re looking for. If our analysis tells us we need to go elsewhere, we will make it happen.

‘In Canada, Montreal is the place that you want to go. It’s the hub in terms of assets under management – all of the big insurers and pension firms are based there – and every time we want to do Canadian roadshows with our local brokers, it’s top of the list and we get a lot of interest from investors there. It’s hard to beat Toronto and Montreal as a two-day road trip combination.’

‘I’m Boston-based, and therefore a lot of the companies that I follow will disproportionately send their management to Boston because they believe, rightly or wrongly, that I have some edge in Boston. But beyond that, companies want to go to New York, number one, Boston, number two. Number three is probably tied between Baltimore and San Francisco or LA and then everything else is decidedly behind that.

‘There’s definitely an increase [in non-US companies coming to visit]. I don’t know how much of that is due to the fact that, when I follow a foreign company, they have less analyst coverage in the US. If you take any big European company, they might be covered by 25 analysts in Europe, maybe more. But in the US, maybe they’re only followed by three or four. And when a foreign company wants to come to the US, the chances are they’re not asking an analyst based in Paris or the UK. We just have greater insight to what’s happening on the ground here: who we talk to about their stock, who’s interested in their stock, who we might suggest being invited to a meeting.'

Findings in this report are taken from the latest round of IR Impact's Global IR Survey, carried out from Q3 to Q4 2024. Any references in this report are for this time period unless stated otherwise. The opening figures featured in the ‘Roadshow overview’ section are based on the total number of respondents who have indicated that they have participated in roadshows, either in person or virtually, over the past year. Any subsequent findings in this report are based on the responses from these roadshow participants only, which means data for both in-person and virtual roadshows includes only respondents who participated in these particular types of roadshows.